The big question!

Why do I have to pay tax in Australia?

“I only earn a pension overseas.”

“I have paid tax on my income in other countries or it wasn’t paid into my account in Australia; it is still in my overseas account.”

Firstly: Are you an Australian resident for tax purposes?

Your residency makes a big difference to how you are taxed in Australia. The Australian Taxation Office (ATO) uses different standards to the Department of Immigration and Border Protection to determine your residency for tax purpose. Because of this, you must ensure that wherever you reside, according to the ATO’s standards, you are taxed (and refunded) appropriately.

Generally, you are considered an Australian resident for tax purposes if you have always lived in Australia or have come to Australia to live. In addition, it also applies to those that have been in Australia for more than half of the income year (unless your usual home is overseas and you don’t intend to live in Australia), or you are an overseas student enrolled in a course of study of more than six months duration. You are also considered a resident for tax purposes if you have moved to Australia from overseas and intend to stay for the foreseeable future and make connections.

Determining residency

To determine your residency for tax purposes, there are a number of tests you can take. The first test is called a resides test. If you reside in Australia, you are considered an Australian resident for tax purposes and you don’t need to apply any other test.

If you don’t satisfy the resides test, you will still be considered a resident if you satisfy one of three statutory tests. These include the domicile test, the 183-day test and the superannuation test.

The domicile test requires you to show that your permanent home is in Australia. If it is, then you are considered an Australian resident for tax purposes.

The 183-day test requires that you have been present in Australia for half the income year (whether continuously or with breaks). If so, you are considered a resident.

The superannuation test is designed to ensure Commonwealth government employees working at Australian posts overseas are treated as Australian residents.

What’s the big deal anyway?

Residency makes a big difference to your tax situation. If you are an Australian resident you are generally taxed in Australia on your worldwide income from all sources. You are also entitled to the tax-free threshold and you must pay a Medicare levy.

If you are not a resident you are generally only taxed in Australia on your Australian-sourced income. Also, you are not entitled to the tax-free threshold. You do not pay the Medicare levy meaning you are not entitled to Medicare health benefits.

Does working overseas change your tax residency?

If you are an Australian resident going overseas to work you will generally remain an Australian resident for tax purposes. Residency is a question of fact that will be determined by your circumstances. You need to show that you have severed your connection with Australia for your status to change.

Your residency status will be considered primarily under the ‘resides’ test and if required the ‘domiciled’ test. The domicile test extends the concept of residence so that a person who is not resident in Australia under the ‘resides’ test may be an Australian resident under the domicile test.

What if your residency status changes?

If your status has changed from resident to foreign resident during the income year, answer ‘yes’ to the question ‘Are you an Australian resident?’ on your tax return.

This ensures you are taxed at resident rates for the tax year. Your foreign residency for part of the year is taken into account by a reduction in your tax-free threshold. You are entitled to a pro-rata tax-free threshold for the number of months you are an Australian resident.

To claim a tax offset for a dependent spouse, you must both be Australian residents for tax purposes. You will need to reduce your claim to take into account the period you were both foreign residents.

Foreign residents do not have to pay the Medicare levy. In your tax return you can claim the number of days in the income year that you are not an Australian resident as exempt days.

From the date you cease to be an Australian resident, there is no need to disclose your foreign-source income in your tax return. Also, all Australian-sourced interest, dividends and royalties derived after you ceased to be an Australian resident are subject to the withholding tax provisions as a final tax and should not be included in your tax return.

Workplace conflict is one of the biggest causes of employee and employer stress and it is no wonder that any disputes should be handled efficiently to prevent harming productivity and damaging team harmony.

Brad, from Acumen Lawyers, provides a case study that looks into handling disputes and useful lessons for employers.

CASE 1 – A dispute between Ms. Luckman and her employer.

Ms. Luckman worked in a permanent part-time capacity for a property management company. Her role involved managing a portfolio of properties, including sales and leasing.

Two disputes arose during Ms. Luckman’s employment:

First Dispute

Ms. Luckman considered that she had a full-time workload although she was working in a part-time capacity. She based this on the amount of properties she was expected to manage.

The dispute was resolved after Ms. Luckman raised this issue with her manager.

Second Dispute

The second dispute arose over a management decision that Ms. Luckman would be managing two new properties in addition to her normal duties.

Ms. Luckman objected to management’s decision on the basis that, although she would be burdened with the responsibility for managing the properties, she would be effectively denied the associated sales commissions because each sale would occur during hours when she was not at work.

Later that day, Ms. Luckman was invited to a meeting with the employer’s General Manager, Mr. Walker.

Meeting – 13 August 2015

During the meeting, Mr. Walker explained the reasons for the decision and advised that he did not consider the transfer of work to her as unusual or uncommon.

Ms. Luckman disagreed with Mr. Walker’s explanation and at the conclusion of the meeting made comments along the lines of “I’m done, I’m over it, I’m out of here”.

Email exchange

After returning to her desk, Ms. Luckman sent Mr. Walker an email which included the following:

“Further to our meeting today, as I feel there is nothing more to discuss, it would be appreciated if the files could now be handed over so I can continue the management of those properties”.

Mr. Walker responded by email which included the following:

“You may feel there is nothing more to discuss, but there is. It’s nothing to lose sleep over but I will make time for us to meet again”.

Dismissal

On 20 August 2015, Ms. Luckman was invited to a further meeting with Mr. Walker.

At the start of the meeting Mr. Walker read out a letter terminating Ms. Luckman’s employment. The letter advised “misconduct” as the reason for Ms. Luckman’s dismissal.

Unfair dismissal claim

Ms. Luckman challenged the termination of her employment by way of an unfair dismissal application to the Fair Work Commission (FWC).

The verdict

The FWC ultimately found the dismissal to have been harsh and unreasonable and thus unfair.

Conduct not inappropriate

The FWC considered that the conduct of Ms. Luckman in the meeting did not amount to a valid reason for her dismissal.

Although observing that Ms. Luckman had been angry and hostile during the meeting of 13 August, the FWC recognised that there had been no use of inappropriate or foul language, or threatening or abusive behaviour, by either party.

The FWC also recognised that Ms. Luckman’s email to Mr. Walker immediately after their meeting demonstrated that she was ready to follow the instruction about the management of the two properties in question.

In particular, the FWC commented:

“The meeting on 13 August 2015 was a robust discussion where an employee had the courage to voice her disapproval over the way that she perceived she had been victimised over the last four years.

The mere fact that there was no swearing or threatening language used solidifies the view that Mr. Walker’s decision to terminate Ms. Luckman’s employment was a monumental overreaction”.

Robust workplace discussions

Importantly for employers, the FWC made the following observation about robust discussions between employers and employees:

“Robust discussions between employees and employers are a part of the Australian industrial landscape.

The notion of master/servant where an employee is not allowed to question the decision of the employer disappeared with the industrial revolution”.

Ultimately, the FWC handed down a decision of unfair dismissal.

As to the question of whether Ms. Luckman could be reinstated, the FWC rejected a claim by the employer that there had been a breakdown of trust in the employment relationship.

Lessons for employers

- Robust workplace discussions between an employer and employee are an accepted feature of the Australian employment landscape.

- An employee may raise a workplace issue directly affecting him/her providing it is raised in an appropriate way.

- Employers are not entitled to deem the mere raising of workplace issue as misconduct or insubordinate behavior.

About the author

Brad Petley is the Principal of Acumen Lawyers, a boutique employment and safety legal practice based in Brisbane but happily solving workplace issues for clients Australia-wide.

Email: brad@acumenlawyers.com.au

This publication is intended only to provide a summary of the subject matter covered. It does not purport to be comprehensive or to provide legal advice. No reader should act or rely on the basis of any matter contained in this publication without first obtaining specific professional advice.

This article is copyright. For permission to reproduce this article please email your request to: info@acumenlawyers.com.au.

July was a great month for markets, continuing a rally that started on the last two days of the financial year. The ASX200 Accumulation index was up 6.29% while the ASX Small Ords Accumulation gained 8.57% during July.

Global shares were a little more modest with the S&P500 up 3.57% in USD terms. The rising Australian dollar, up 1.87% during the month, shaved international returns as measured by the MSCI World Total Return index (AUD) back to 2.13% for July.

The Australian dollar rally must be frustrating for the RBA right now. Reading the notes that accompanied the cut from 1.75% to 1.50% on August 2, you find a passing mention of the currency however, it seems likely to have been a big factor in dropping the rate. The rate cut itself was not a big surprise, nor the action by banks to pass on only a portion of the cut to borrowers. No, the big surprise was that term deposit rates were not cut by the same amount. Could it be that someone is getting the message that conservative retired savers, who may not have been the world’s ‘big spenders’ in recent history, are really starting to pull in the belt as income available from term deposits shrinks to all-time lows?

The comments by Glenn Stevens in his final speech as Reserve Bank Governor seem to have revealed more of what he was thinking than the sterile rate cut announcement. He focused on issues that ought to be the focus of grown up political debates by politicians of all stripes, yet get buried under the day to day opportunistic sniping. He mentioned debt-laden households who are reluctant to spend, which in turn makes it harder to stimulate. These households, when delivered a rate cut and faced with uncertainty, seem more likely to use the benefit to pay down debt, rather than spend. This has made monetary policy (pulling the interest rate levers) less effective than in the past.

The quality of government deficit spending was also put into focus. In his appeal that governments do more to stimulate the economy, he was not advocating ‘helicopter money’, as delivered by Kevin Rudd, and he also warned against being complacent in borrowing to fund day to day government outlays. His focus was on the government replenishing the stock of long-lived investment assets that produce an economic return. I think everyone agrees that deficit spending on such projects is in everyone’s interest. My thoughts – not his – would such a productive asset be a football stadium, or a new export facility for live cattle? A casino, or a railway line? Governments really need to think hard about how to get the most bang for buck out of any deficit spending. Mr Stevens did conclude by saying that we had better start having these hard conversations before the next crisis.

Turning to world events (not the US election – there will be plenty of time for that in the next few months), a sector that carries potential contagion effect is the European banking system.

Will the Italian banks become the ‘scene of the accident’ that triggers the next crisis?

There is no doubt that the Italian banking system is in need of additional capital. More than a third of Monte dei Paschi’s loans are non-performing, and it sits at the bottom of the table of 51 European banks in the latest ‘stress testing’. The Italian economy is smaller now than it was 16 years ago. And opportunities to improve productivity, while they exist, are unlikely to be grasped by a government that ranks as the least effective in all of Europe.

The vexing question is who will stump up for new shares to expand the bank’s core risk capital?

There are three candidates: governments, new shareholders, or existing holders of hybrid bonds.

Unfortunately, EU rules allow state government bail-outs only if holders of hybrid securities are also ‘bailed in’. That is to say, the holders of those hybrid bonds take a loss on their securities as they are converted to equity in order to ‘re-capitalise’ the banks. In that case, the governments and the existing holders of hybrids share the pain. It is unlikely that new shareholders would be voluntarily pumping new money into these institutions with such a large book of impaired assets. Could Monte dei Paschi become Europe’s Lehmann Brothers?

We don’t know the answer, but it is on our minds as we position portfolios. However, it does lead us to another topic current in financial markets in July; Bank bashing.

The announcement of a $9.2 billion profit at CBA poured more fuel on the fire of the haters who are convinced of the need for a royal commission. While $9.2 billion is a big profit, it needs to be seen in the context of how much the company is worth, and the total value of its loans.

The value of all the CBA shares on the market today is $132 billion. So the $9.2 billion profit equals just 6.9% return on investment after tax on the current value of the shares held by hundreds of thousands of shareholders (yes, including those industry superfunds) who own CBA shares.

The value of all assets held by CBA (the vast majority being loans to homeowners) equals $933 billion. In context then, the $9.2 billion after tax profit represents a profit after tax and expenses of around 0.98% on those ‘assets’.

The final ratio to comment on is return on equity. This is the profit divided by the paid up equity capital within the bank. This ratio is 15.7% which, like the other Australian banks, is amongst the highest in the world. However, demands from global banking regulators, for all banks to hold more shareholder capital, will result in lower returns as profits are spread across a larger capital base. Macquarie bank forecasts that CBA’s return on equity will decline to 14.3% by 2019.

The upshot is, would we prefer a banking sector like the one we have in Australia or would something more akin to the Italian model be more to the public liking? Stable and trustworthy financial services are the lifeblood of a vibrant economy and the aggregate benefits from banks making a quarter of a percent more on loans than their global peers is likely to outweigh the cost of a banking system regulated out of existence.

Market valuations

The recent run up in the ASX200 to around 5500 has pushed valuations to a level above historical norms. At this level, the market trades at 16.8 times the expected 2017 earnings. With interest rates low, the case can be made that equities are fair value at these levels. However, the earnings outlook is subdued at best and we think that a trading range of 5100 to 5700 is likely to contain the market for the rest of the year.

In the US, markets have broken out above the highs from May 2015 and are in all-time high territory. The S&P500 trades at 17.2 times what analysts expected 2017 earnings (Factset consensus). When looking at trailing actual earnings, which declined by 3.5% over the last year, the ‘as reported’ P/E multiple is 24 times.

At these levels, markets are not cheap and we have equity holdings at lower than normal levels. The problem for investors is that there are few attractive alternatives and the temptation is to go all-in. We don’t advocate trying to time the market with an all-in or all-out position, but it is good to be aware of market cycles, and keeping some cash on the sidelines whenever prices get expensive.

In most cases, the banks expect a 20% upfront deposit before they will consider approving you for a home loan. A 20% deposit for the Australian median house price of $660,000 equals $132,000! Fortunately for those of us living in Brisbane, the median house price here is just over $510,000. Unfortunately, that still means we are required to cough up $102,000 as a deposit!

For most of us, saving that kind of cash and purchasing a home in our 20s is almost impossible. According to recent reports, 57% of first home buyers are now aged between 30-40 years old.

How can Lenders Mortgage Insurance help?

The banks do however offer Lenders Mortgage Insurance (LMI) if you are unable to produce the full 20% deposit. However, this is not to be mistaken as insurance for you. LMI is security for the lender to ensure that they will not incur a loss should you default on your home loan. This is why banks request a 20% deposit prior to considering your loan.

The cost for LMI is most commonly added to your home loan. It is important to understand that once LMI is added to your home loan principal, you will be paying interest on top of the LMI amount and your minimum regular repayments will increase accordingly.

Alternatively, if you are fortunate enough to have parents (or a close relative) with equity in their own home, they may be eligible to become a guarantor for you. Becoming a guarantor on a loan essentially means becoming the security on the home owner’s loan. This is a strategy to avoid the cost of LMI if you have not saved the 20% required for a deposit. However, if you default on your home loan, your guarantor will be liable to repay the portion of the home loan they have become guarantor on. Most banks request the guarantor to seek financial advice before committing to this strategy.

To assist and encourage Australians to save towards their first home, the government has previously offered first home owners saving accounts. These had great incentives including an additional contribution of 17% for the first $6,000 deposited each financial year. Unfortunately, the government abolished these accounts as of 1 July 2015 and apart from the First Home Owners’ Grant, the government does not offer any other schemes to help first home owners.

Tips for saving a deposit

There are a couple of strategies you might consider to make saving for a deposit easier:

The Fixed Interest Approach: Through careful budgeting and serious consideration of your current spending habits, you may be surprised at just how much you can save. Is that coffee on your way to work really necessary, or could you perhaps make one at home and pop it in a travel mug? Is the Diet Coke you purchase each time you fill up your car really worth it? ASIC’s Money Smart have a useful budgeting tool called “TrackMySPEND” which could help you develop a personalized budget.

Bear in mind that careful budgeting and strict discipline go hand in hand. If you find yourself spending everything you earn, it might be a good idea to open a high interest savings account with low fees. Each time your pay is deposited into your everyday bank account, your first priority should be to transfer your savings straight into that high interest savings account, and leaving it there. You could even set up an automatic transaction so you don’t have to think about it.

Please carefully read the Product Disclosure Statements before opening any new accounts. High interest savings accounts may incur a fee if more than one withdrawal is made per month, and in some cases, you may lose your high interest rate for that month if withdrawals are made.

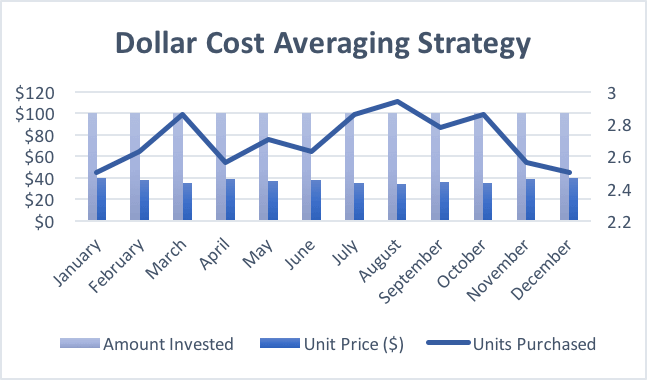

The Investment Approach: If you don’t mind a little bit of risk, this could be a viable option to consider. Investment strategies such as Dollar Cost Averaging (DCA) can dramatically increase your wealth over time. The purpose of this strategy is to reduce market timing risk. This essentially means that you are avoiding purchasing a lump sum of units at their peak price, but rather investing gradually over time to average out the price per unit.

The below table illustrates the benefit of Dollar Cost Averaging when $100 per month has been invested over a 12-month period.

| Month | Amount Invested | Unit Price ($) | Units Purchased |

| January | $100 | 40 | 2.5000 |

| February | $100 | 38 | 2.6316 |

| March | $100 | 35 | 2.8571 |

| April | $100 | 39 | 2.5641 |

| May | $100 | 37 | 2.7027 |

| June | $100 | 38 | 2.6316 |

| July | $100 | 35 | 2.8571 |

| August | $100 | 34 | 2.9412 |

| September | $100 | 36 | 2.7778 |

| October | $100 | 35 | 2.8571 |

| November | $100 | 39 | 2.5641 |

| December | $100 | 40 | 2.5000 |

| Total | $1,200 | 32.3844 |

Total Amount Invested: $1,200

Total End Value: $1,295*

Gross Capital Gain: $95

*Total Units Purchased X End Value Per Unit (rounded)

At the end of the investment period, the investor has increased their portfolio value by $95 without the unit price ever increasing more than the starting price.

Dollar Cost Averaging could be a suitable strategy for those who may have a tight budget or for those that are in no rush to get into the property market but are aiming to own their own home one day. However, it is important to understand the type of portfolio you are investing in.

Typically, balanced investors will let their portfolios grow for a minimum of 3 years before withdrawing any funds. On the other hand, those who are investing in more growth type assets (such as international shares) tend to let their portfolio grow for a minimum of 5-7 years before withdrawing any funds. The purpose of these timeframes is to allow the investments to run their natural course.

It is important to clearly understand your tolerance towards risk before considering this strategy. To discuss this in further detail, contact Quill today.

What impacts your borrowing power

While saving towards your deposit is essential for banks to seriously consider your eligibility for a home loan, other factors may impact your borrowing power. Credit card debt or a personal loan or car loan, may heavily impact on how much the bank will lend you. 10 years ago, my brother and his wife applied for a home loan and discovered that because of their $15,000 car loan, their borrowing power was reduced by approximately $80,000!

Generally, all banks will also require a credit history check. When I first spoke to the bank about applying for a home loan, they instructed me to take out a credit card as I had never had any debt before and therefore had no credit history.

Reducing or, even better, eliminating your current debt now will better prepare you for when you apply for a home loan. Strategizing how best to make your repayments plus increasing your savings can be a daunting task. But with a plan in place and strict discipline, it’s not impossible.

Please note, this is general advice only and does not take into account your personal circumstances. If you would like to find out the best strategy for you, or if you would like some extra tips, contact Quill today and start building your house deposit!

The Australian Taxation Office (ATO) has warned it is focusing more on taxpayers earning money from the sharing economy this tax time. The ATO has cautioned that it has in excess of 600 million pieces of third party data to track activity and income.

What is the sharing economy?

A sharing economy is one that connects buyers (users) and sellers (providers) through an enabler who usually operates an app or a website. Uber and Airbnb are examples of these popular sharing economy companies, driven by advances in technology. People that provide goods or services through such operators need to consider how GST and income tax apply to their earnings.

What is Tax Audit Insurance and how can it help?

The ATO and other government bodies continue to target individuals and businesses and are scrupulously pursuing taxpayers though their data matching ability.

With this in mind, Quill Group have in place a Tax Audit Insurance arrangement, underwritten by AAI Limited trading as Vero Insurance (a subsidiary of Suncorp Group Limited). This is designed to cover the professional fees incurred with the preparation of material and management of the response process. Despite honest and thorough declarations, taxpayers can still be targeted for an audit, enquiry, investigation or review by the ATO.

This is designed to cover the professional fees incurred with the preparation of material and management of the response process. Despite honest and thorough declarations, taxpayers can still be targeted for an audit, enquiry, investigation or review by the ATO.

The costs incurred with audits and such investigations can be significant even if lodgements are correct and no further adjustments are made. It is a common misconception that you will only be audited if you are not compliant. However, there is strong evidence to show that the ATO has reviewed many returns where no adjustments were required to be made.

As professionals, Quill can respond to queries and provide information to explain your position and we bring a skill in communicating with these government departments to advocate for your position. This means you can relax, knowing we are on your side and your costs are covered.

How do I get this insurance?

Our Audit Shield letters will be going out this month. They will include the Client Acceptance Forms, making it possible for our clients to take up this cover by the 31st August, or renew cover if already utilising this Quill service. These fees are tax deductible.

Should you have any queries relating to Audit Shield please call us to discuss.

Claim Donations

Coming up to the end of the financial year it is a good idea to start looking for the donations you have already made or the ones you can contribute to now – and how your can claim them. Michelle Gargar talks about charities to look out for and which ones you can claim in our Money Matters segment.

Financial markets have seen a fair share of volatility in recent months. The most recent was the unexpected Brexit vote which sent currencies both soaring and plummeting as well as creating renewed interest in gold. When all the dust settled, as it has in the last few days, markets returned to where they were before the event, the exception being currency relationships with the UK Pound.

The 2016 financial year surprised on many different fronts. US interest rates rose, but only by a quarter of a percent, and the long awaited economic recovery which was the premise for interest rate rises, has remained as elusive as ever. As a result, the interest rate sensitive sectors continued to outperform. The Australian Bloomberg Composite Bond index rose 7.02% which created another year in which investors who are dubious of the value of investing in bonds with interest rates at 500 year lows were wrong again. Other big beneficiaries were Utilities, with that sector up 25.5% over the last twelve months. Australian listed property trusts (A-REIT’s) also had a tearaway year gaining 24.5%. A little truism to keep in mind here is that ‘trees don’t grow to the sky’ and there does reach a point where some of these asset classes that have had their day in the sun, might well have many a year in the shade.

Meanwhile, with the global economy sputtering and profits falling, equity markets generally have finished the year where they started. The S&P/ASX200 Accumulation index was up a mere 0.56% for the year, and the MSCI World index in AUD was up only 0.96%. Those seemingly benign numbers though mask the intra year volatility, which has seen an 18% range for the ASX, and a 16% range for the US markets.

Our strategy has not changed. Seek out the quality. Invest in assets that are appropriate for your time frames. Ignore the noise. Don’t get spooked out of markets at the very bottom. (easier said than done – but see our Brexit update for an example of that advice) Don’t get too carried away when markets have a good run. Remember the proverb – ‘this too shall pass’.

Financial institutions, as part of their obligations under the Foreign Account Tax Compliance Act (FATCA) are now starting to contact customers after they have performed a review of their accounts to determine whether these accounts are held by US citizens, US tax residents, US entities, or non-US entities controlled by US persons. FATCA was enacted to improve compliance with US tax laws. FATCA imposes certain due diligence and reporting obligations on foreign (non-US) financial institutions, including Australian institutions. These institutions will be required to report to Australian Taxation Office (ATO) information on US citizens with financial accounts. The information reported to the ATO will then be passed on to the IRS.

Should your bank contact you, you may receive a FATCA Self Certification Declaration from your bank/financial institution similar to the Suncorp form attached.

Please contact our office should you have any questions.

Back in mid-February, we published an article that responded to the ‘bear market’ status that had just been achieved by the ASX200. In it we warned against knee-jerk reactions and selling down, just on the basis of a ‘label’ that acknowledges that markets are down by 20%. We further postulated on the possibility of a quick 10% rally from that point, as had happened in previous bear markets, and the impact this might have on creating a double mistake for investors.

Since then we have seen the ASX200 Accumulation index up almost 15% in a little over three and a half months. Selling in reaction to ‘bear market’ status was clearly the wrong thing to do. Timing of any sort of perfection is very difficult. Not to say that we don’t consider valuation and risk, we certainly take these factors into account when setting tactical asset allocations, but big bets, either way, are likely to produce disappointing results. Better a live dog than a dead lion, so the proverb goes.

The ‘dis-inflation’ theme continued to play out in April as the March Quarter CPI numbers surprised on the downside, and the RBA followed that up with a cut to the Official Cash Rate. Our comments on the date of the cut suggested that if the AUD/USD level of $0.755 was broken we would see even more downside. That has come to pass with the AUD since hitting a low of $0.7144 in late May.

The surprise CPI number led to some notable changes to predictions of interest rates. Macquarie Bank has adjusted their expectations and see interest rates falling to 1.00% before this cycle of cuts bottoms out. JP Morgan’s Sally Auld sees rates down to 1.00% by mid-2017. Over at CBA, the expectation is that rates will fall to 1.25% by November this year. National Bank still have a 1.75% bottom, and see this lasting through until mid-2018, that’s another two years away before any increase. If any of these are near the mark, and if we do see two rate rises by the US Federal Reserve this year, then we could expect the AUD to trade well under $0.70 for most of the next twelve months.

Against this backdrop of lower rates, with economic activity that weak but not exactly collapsing, assets with yield will continue to be attractive. Low rates and easier credit have resulted in booming apartment construction, and that sector will see some price weakness as investors feel the reality of an oversupply and lack of willing tenants. However, real estate, where yields are 5% plus, will still be attractive, as long as tenant demand has a reasonably low correlation to economic activity.

With the rally in equities, we are looking to lighten up on exposures, and clients with managed portfolios will see a move to fund managers that have a history of risk aversion. We are also introducing investors to some other alternative funds with low equity market correlations.

Big political catalysts remain on the horizon this year, including the Brexit vote in the UK on June 23, our own elections on July 2, and of course the US Federal elections in November. We pass no comment on the US candidates except to say that on both sides the thinkers are clearly outnumbered by the populists, and it looks like:

“two wolves and a lamb voting on what to have for dinner” – Hat tip to James Bovard.

As we continue to expand the use of online services, we must make sure that we keep data security in the forefront of our mind. Whether you log on to your online banking on a communal computer or are the target of a phishing scam, opportunistic criminals are always trying to access your sensitive information.

With the cloud seemingly taking over our data storage in so many areas, we especially need to keep up to date with ways of keeping our data our own.

Xero has recently given its users the opportunity to improve the protection of their financial data, by offering a two-step authentication process when logging on to your account. This is an opt-in service requiring users to enter their original username and password as well as a randomly generated six-digit code to log in.

How do you enable Xero Two-Step Authentication?

The team at Xero have created a video, which shows how easy it is to set up.

https://www.xero.com/nz/tv/video/11350-two-step-authentication-for-xero/

By using this feature you will also be able to view your recent login history, which shows the location and time of your past logins. This will mean you can determine if there are any suspicious logins into your account. If you see any unusual activity you can contact support directly from this screen.

We suggest you use this if you are using mobile devices which could easily be left behind, or if you are logging into various computers from time to time.

You do have the option to “Remember me for 30 days” on the machine or browser you usually log onto which means you only need to enter the authentication every 30 days. If you can’t use the app you can answer a series of security questions also.

Other applications which Two-Step Authentication can be applied.

Many other applications offer two-step authentication and include but are not limited to:

- Dropbox,

- Paypal,

- LinkedIn,

- Gmail and

Two-step authentication is the future. With all of our data and personal information being stored online, it is necessary and wise to have some sort of protection in place.