For most people, deciding what should be done with their assets and possessions after they die is not something they like to consider. Although it is a bit morbid, this decision is extremely important to ensure your carefully earned assets are distributed according to your wishes. While most people bequest their house, household contents, jewellery, collectibles, cars, boats, and things of that nature in their will, their superannuation and pension balances are often forgotten. This is where superannuation death benefit nominations become extremely important.

What steps can you take?

Superannuation fund trustees allow members to make what is called a ‘death benefit nomination’ for their account balances. This nomination allows members to dictate to the superannuation fund trustees where their superannuation benefits should be paid if the member passes away. However, it should be noted that there are different types of death benefit nominations and not all superannuation providers offer all options. The governing rules of superannuation funds define whether they can allow certain types of death benefit nominations to be made.

There are two types of death benefit nominations: binding and non-binding. Both are only activated on the superannuation members’ death and are usually paid in lump sums to the beneficiaries.

Binding death benefit nominations

A binding death benefit nomination binds the superannuation trustee to paying the members’ superannuation benefits as directed by the member before their death. However, binding nominations can still be overruled by the superannuation fund trustee in some cases.

Binding nominations expire every 3 years. While having to provide a new nomination every 3 years may seem like a hassle, consider how much your life may change in 3 years by births, deaths, separation, divorce or marriage etc. When this is taken into account, updating your death benefit nomination every 3 years seems like a prudent measure.

Non-binding death benefit nominations

A non-binding death benefit nomination is similar to a binding death benefit nomination, except the superannuation trustee is not bound to pay your superannuation benefits to your nominated beneficiaries. You are able to nominate who you would prefer your benefits to be paid to, however, this is used as a guide and the ultimate decision remains with the superannuation trustee. The trustee must still pay the benefits to a dependent or your legal personal representative however.

Non-lapsing binding death benefit nominations

These are much the same as binding death benefit nominations but with one crucial difference – this nomination remains in place until you revoke it, change it or make a new nomination. This may present a trap if you nominated your beneficiaries when you first opened your superannuation account 10 years ago but have not checked or updated your nomination since then.

If you were to pass away before updating your nomination, your superannuation benefits might not be paid the way you intended. It’s worth checking your nomination often to ensure your beneficiaries are up to date. This information is usually recorded on the annual statement provided by your superannuation fund at the end of every financial year.

Reversionary nominations

Reversionary nominations are another type of death benefit nomination specifically in relation to a pension or annuity. It simply means that on your death, the regular payment amount from your pension or annuity would continue to be paid to an individual nominated by you.

If the rules of the superannuation fund allow it, you could nominate your beneficiaries via a binding or non-binding death benefit nomination instead of a reversionary nomination, however, the benefit would be paid as a lump sum, not a regular income stream. It’s also worth noting that not all beneficiaries can receive a superannuation death benefit as an income stream.

Self-managed superannuation funds

Self-managed superannuation funds are able to make binding death benefit nominations, however, they are bound by rules and limitations according to the ATO Self-Managed Superannuation Funds Determination 2008/3.

What happens if no binding nomination is in place?

If a member has no binding nomination in place or has let their nomination lapse, the superannuation fund trustee may consider any valid non-binding death benefit nominations the member made before their death when deciding where to pay the member’s superannuation benefits. The trustee will also make enquiries about the member’s will and family situation before paying the benefits, however, the superannuation fund trustee must pay the death benefits in accordance with the superannuation fund’s trust deed rules as well as the governing rules of the superannuation fund, superannuation law, and common law.

Who can be a beneficiary?

Your beneficiaries/beneficiary must be a dependent of you or they must be your legal personal representative (LPR). This is usually the executor of your will or your estate administrator. You are able to nominate multiple beneficiaries with different allocations but the total allocation must equal 100%. You are able to allocate part of your benefits to your LPR with the remaining portion going to a beneficiary.

The SIS Act 1993 classifies a dependent as one of the following:

- Your spouse or de-facto spouse

- Children, including adopted, ex-nuptial and stepchildren of any age

- A person who was financially dependent and reliant on you at your death

- An individual who has a close personal relationship with you. This person must live with you and one or both of you must provide the other with financial support, domestic support, and personal care. They do not have to be related to you.

Making a valid nomination

For a death benefit nomination to be valid, all of the following criteria must be met:

- Nomination is made in writing by the member

- Beneficiary is a dependent according to the SIS Act 1993 or is the LPR of the member

- Allocations are clear and all required details have been provided

- Nomination has been signed and dated by the member in the presence of 2 witnesses over the age of 18

- Nomination must be reviewed at least every 3 years

Checking that the death benefit nominations on your superannuation funds are up to date will ensure that your carefully accumulated superannuation benefits are paid to the right people after you are gone.

For help on nominating your beneficiaries or making a death benefit nomination, contact Quill Group today. Quill Group also has in-house estate planning lawyers based on the Gold Coast through our subsidiary company Intello Legal.

Other articles related to binding death benefit nominations

The following are other articles related to superannuation estate planning which may be of interest:

- The importance of estate planning

- Is your SMSF estate plan up to speed?

- Wills and SMSF estate planning (Intello)

Do you catch the bus to work? Are you caught up on the new tax rules?

The Australian Taxation Office (ATO) has released a ruling that would allow employees to salary package the cost of getting to and from work later this year (this only applies to bus travel so no train or city cat on the cards as yet!).

This will be available via employers or certain salary packaging providers like RemServ who have obtained a private ruling from the ATO. This benefit will be available on the TransLink network within South East Queensland (from Gympie down to Coolangatta and west to Helidon).

This will allow eligible employees to pay for their bus travel with pre-tax dollars, reducing their taxable income resulting in less tax to pay. The new TransLink smart card will be topped up with pre-tax dollars when the balance falls below $5 and can be used just like a regular go card.

RemServ has estimated that those who earn $70,000 per year and take 10 trips a week across four zones could save just under $1,500 a year under the plan – that’s a latte every day!

If you would like to know more about this scheme, please contact our office.

The Australian Taxation Office (ATO) generally imposes interest on unpaid tax liabilities including Income Tax, GST, FBT, and PAYGW to name a few. The ATO is fairly lenient in imposing interest or penalties on your tax liability for late payments. However, they are not as fair when the late payments or lodgements are multiple and continuous. The key to dealing with the ATO is regular communication and keeping them updated.

For the July 2016 quarter, the ATO’s General Interest Charge (GIC) rate is 9.01% p.a. Note that there are two types of interest charged by the ATO:

- General Interest Charge (GIC) – penalty for late payment and other obligations

- Shortfall Interest Charge (SIC) – usually a penalty from tax return amendment resulting to an increase of tax liability

Penalties imposed on tax accounts

The purpose of penalty provisions is to encourage taxpayers to take reasonable care in complying with their tax obligations. The ATO does take into account individual circumstances such as compliance history when deciding what action to take. This means that ‘regular offenders’ could receive stricter treatment than what a ‘first-timer’ would.

From the above penalties and interest charges that the ATO can impose on a taxpayer’s account, there are basic grounds and circumstances that the Commissioner may remit GIC, SIC or penalty.

Every taxpayer has the right to request remission of any interest imposed to their account. Remission is the reduction or cancellation of interest charged on the taxpayers account. The ATO generally remits interest charges and penalties where it is fair and reasonable in the circumstances.

Whether you are requesting remission over the phone, through the ATO Portal or via mail, we have listed common circumstances taxpayers face that lead to the need for remission:

- The tax shortfall amount occurred as a consequence of voluntary disclosure by the taxpayer

- The ATO’s completion time of an audit took longer than could reasonably be expected taking into account specific circumstances

- The ATO has, by instruction or action, contributed to the taxpayer’s error giving rise to shortfall

- Delays were caused by, and errors due to, the actions of a third party (i.e. incorrect information provided by a third party)

The last scenario, above, is an overly used reason in requesting remission. This is because the shortfall is outside the control of the taxpayer.

Requesting a remission for SIC is one of the more difficult to achieve, especially if it was detected during the ATO’s data matching. SIC can be easily granted by the Commissioner if the result of increase in tax liability was initiated by the taxpayer and the ATO were notified that a mistake had been made.

There are also other different grounds and circumstances where the ATO may remit interest and penalties. These are discussed in more detail in Practice Statement Law Administration PS LA 2006/8.

If you are unsure about your reason for remission, please contact Wendy from our office and she can assist you with this process and provide further information.

The big question!

Why do I have to pay tax in Australia?

“I only earn a pension overseas.”

“I have paid tax on my income in other countries or it wasn’t paid into my account in Australia; it is still in my overseas account.”

Firstly: Are you an Australian resident for tax purposes?

Your residency makes a big difference to how you are taxed in Australia. The Australian Taxation Office (ATO) uses different standards to the Department of Immigration and Border Protection to determine your residency for tax purpose. Because of this, you must ensure that wherever you reside, according to the ATO’s standards, you are taxed (and refunded) appropriately.

Generally, you are considered an Australian resident for tax purposes if you have always lived in Australia or have come to Australia to live. In addition, it also applies to those that have been in Australia for more than half of the income year (unless your usual home is overseas and you don’t intend to live in Australia), or you are an overseas student enrolled in a course of study of more than six months duration. You are also considered a resident for tax purposes if you have moved to Australia from overseas and intend to stay for the foreseeable future and make connections.

Determining residency

To determine your residency for tax purposes, there are a number of tests you can take. The first test is called a resides test. If you reside in Australia, you are considered an Australian resident for tax purposes and you don’t need to apply any other test.

If you don’t satisfy the resides test, you will still be considered a resident if you satisfy one of three statutory tests. These include the domicile test, the 183-day test and the superannuation test.

The domicile test requires you to show that your permanent home is in Australia. If it is, then you are considered an Australian resident for tax purposes.

The 183-day test requires that you have been present in Australia for half the income year (whether continuously or with breaks). If so, you are considered a resident.

The superannuation test is designed to ensure Commonwealth government employees working at Australian posts overseas are treated as Australian residents.

What’s the big deal anyway?

Residency makes a big difference to your tax situation. If you are an Australian resident you are generally taxed in Australia on your worldwide income from all sources. You are also entitled to the tax-free threshold and you must pay a Medicare levy.

If you are not a resident you are generally only taxed in Australia on your Australian-sourced income. Also, you are not entitled to the tax-free threshold. You do not pay the Medicare levy meaning you are not entitled to Medicare health benefits.

Does working overseas change your tax residency?

If you are an Australian resident going overseas to work you will generally remain an Australian resident for tax purposes. Residency is a question of fact that will be determined by your circumstances. You need to show that you have severed your connection with Australia for your status to change.

Your residency status will be considered primarily under the ‘resides’ test and if required the ‘domiciled’ test. The domicile test extends the concept of residence so that a person who is not resident in Australia under the ‘resides’ test may be an Australian resident under the domicile test.

What if your residency status changes?

If your status has changed from resident to foreign resident during the income year, answer ‘yes’ to the question ‘Are you an Australian resident?’ on your tax return.

This ensures you are taxed at resident rates for the tax year. Your foreign residency for part of the year is taken into account by a reduction in your tax-free threshold. You are entitled to a pro-rata tax-free threshold for the number of months you are an Australian resident.

To claim a tax offset for a dependent spouse, you must both be Australian residents for tax purposes. You will need to reduce your claim to take into account the period you were both foreign residents.

Foreign residents do not have to pay the Medicare levy. In your tax return you can claim the number of days in the income year that you are not an Australian resident as exempt days.

From the date you cease to be an Australian resident, there is no need to disclose your foreign-source income in your tax return. Also, all Australian-sourced interest, dividends and royalties derived after you ceased to be an Australian resident are subject to the withholding tax provisions as a final tax and should not be included in your tax return.

Before turning the ripe age of 30, I had never appreciated the importance of having a “good” accountant. Up until then it was just about “get me a good refund”. I never respected the extensive years of study involved and the importance of their role in our daily lives.

Don’t get me wrong, I’m not putting everyone in this category but I know personally, my friends and I never spoke a word about accounting except for the once a year call: “I got my refund back – lets party”.

How naive we were.

Nowadays, we are buying houses, we are investing, we are looking at share markets, we are starting small businesses and we are literally planning for our family’s future.

Turns out that building a relationship with your accountant is imperative for your business to grow and be successful. The right person can save you time and money.

Below are my tips for things to consider when choosing an accountant:

Location – are you willing to travel or collaborate electronically through email or by phone?

Competitively priced – find out up front what the fees will be. Ask for a quote.

Software – Do they use modern, up to date accounting programs? Will you need cloud-based accounting? Don’t be put off straight away by technology as it can save you money by making things more efficient.

Do your research Ask friends for referrals. Everyone loves a good Google search.

What qualifications do they have? Check what qualifications and certifications your accountant has. Greater experience and knowledge can mean extra value is added to your business as opposed to a ‘backyard job’. Be cautious of super cheap backyard jobs as they can cause you bigger headaches in the long run.

The accountant you choose should be capable and accountable for meeting your business and/or personal needs. If you choose the wrong accountant, the chances of missing out on important information could turn out very costly for yourself or your business.

Remember, this is a long-term relationship that you are getting into. If you and your accountant don’t get along or don’t see eye to eye, the fallout could be disastrous and impact negatively on your business.

Be prepared. I already mentioned the extensive study that accountants undertake, however, I’m almost certain ‘mindreading’ wasn’t one of the subjects studied in their university degree. Ask for checklists so that you can supply all relative information on time.

Don’t push this to the side; it’s not as daunting as you think– knowing exactly what position your business is in will then create more opportunities for you and your accountant to better your business position and open up innovative avenues for the business to go down.

In this case growing up isn’t so bad!

In most cases, the banks expect a 20% upfront deposit before they will consider approving you for a home loan. A 20% deposit for the Australian median house price of $660,000 equals $132,000! Fortunately for those of us living in Brisbane, the median house price here is just over $510,000. Unfortunately, that still means we are required to cough up $102,000 as a deposit!

For most of us, saving that kind of cash and purchasing a home in our 20s is almost impossible. According to recent reports, 57% of first home buyers are now aged between 30-40 years old.

How can Lenders Mortgage Insurance help?

The banks do however offer Lenders Mortgage Insurance (LMI) if you are unable to produce the full 20% deposit. However, this is not to be mistaken as insurance for you. LMI is security for the lender to ensure that they will not incur a loss should you default on your home loan. This is why banks request a 20% deposit prior to considering your loan.

The cost for LMI is most commonly added to your home loan. It is important to understand that once LMI is added to your home loan principal, you will be paying interest on top of the LMI amount and your minimum regular repayments will increase accordingly.

Alternatively, if you are fortunate enough to have parents (or a close relative) with equity in their own home, they may be eligible to become a guarantor for you. Becoming a guarantor on a loan essentially means becoming the security on the home owner’s loan. This is a strategy to avoid the cost of LMI if you have not saved the 20% required for a deposit. However, if you default on your home loan, your guarantor will be liable to repay the portion of the home loan they have become guarantor on. Most banks request the guarantor to seek financial advice before committing to this strategy.

To assist and encourage Australians to save towards their first home, the government has previously offered first home owners saving accounts. These had great incentives including an additional contribution of 17% for the first $6,000 deposited each financial year. Unfortunately, the government abolished these accounts as of 1 July 2015 and apart from the First Home Owners’ Grant, the government does not offer any other schemes to help first home owners.

Tips for saving a deposit

There are a couple of strategies you might consider to make saving for a deposit easier:

The Fixed Interest Approach: Through careful budgeting and serious consideration of your current spending habits, you may be surprised at just how much you can save. Is that coffee on your way to work really necessary, or could you perhaps make one at home and pop it in a travel mug? Is the Diet Coke you purchase each time you fill up your car really worth it? ASIC’s Money Smart have a useful budgeting tool called “TrackMySPEND” which could help you develop a personalized budget.

Bear in mind that careful budgeting and strict discipline go hand in hand. If you find yourself spending everything you earn, it might be a good idea to open a high interest savings account with low fees. Each time your pay is deposited into your everyday bank account, your first priority should be to transfer your savings straight into that high interest savings account, and leaving it there. You could even set up an automatic transaction so you don’t have to think about it.

Please carefully read the Product Disclosure Statements before opening any new accounts. High interest savings accounts may incur a fee if more than one withdrawal is made per month, and in some cases, you may lose your high interest rate for that month if withdrawals are made.

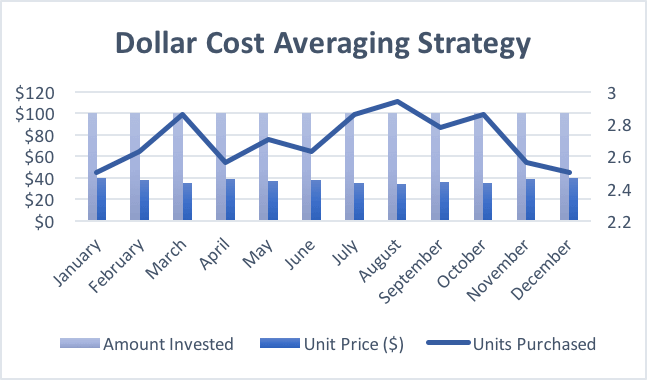

The Investment Approach: If you don’t mind a little bit of risk, this could be a viable option to consider. Investment strategies such as Dollar Cost Averaging (DCA) can dramatically increase your wealth over time. The purpose of this strategy is to reduce market timing risk. This essentially means that you are avoiding purchasing a lump sum of units at their peak price, but rather investing gradually over time to average out the price per unit.

The below table illustrates the benefit of Dollar Cost Averaging when $100 per month has been invested over a 12-month period.

| Month | Amount Invested | Unit Price ($) | Units Purchased |

| January | $100 | 40 | 2.5000 |

| February | $100 | 38 | 2.6316 |

| March | $100 | 35 | 2.8571 |

| April | $100 | 39 | 2.5641 |

| May | $100 | 37 | 2.7027 |

| June | $100 | 38 | 2.6316 |

| July | $100 | 35 | 2.8571 |

| August | $100 | 34 | 2.9412 |

| September | $100 | 36 | 2.7778 |

| October | $100 | 35 | 2.8571 |

| November | $100 | 39 | 2.5641 |

| December | $100 | 40 | 2.5000 |

| Total | $1,200 | 32.3844 |

Total Amount Invested: $1,200

Total End Value: $1,295*

Gross Capital Gain: $95

*Total Units Purchased X End Value Per Unit (rounded)

At the end of the investment period, the investor has increased their portfolio value by $95 without the unit price ever increasing more than the starting price.

Dollar Cost Averaging could be a suitable strategy for those who may have a tight budget or for those that are in no rush to get into the property market but are aiming to own their own home one day. However, it is important to understand the type of portfolio you are investing in.

Typically, balanced investors will let their portfolios grow for a minimum of 3 years before withdrawing any funds. On the other hand, those who are investing in more growth type assets (such as international shares) tend to let their portfolio grow for a minimum of 5-7 years before withdrawing any funds. The purpose of these timeframes is to allow the investments to run their natural course.

It is important to clearly understand your tolerance towards risk before considering this strategy. To discuss this in further detail, contact Quill today.

What impacts your borrowing power

While saving towards your deposit is essential for banks to seriously consider your eligibility for a home loan, other factors may impact your borrowing power. Credit card debt or a personal loan or car loan, may heavily impact on how much the bank will lend you. 10 years ago, my brother and his wife applied for a home loan and discovered that because of their $15,000 car loan, their borrowing power was reduced by approximately $80,000!

Generally, all banks will also require a credit history check. When I first spoke to the bank about applying for a home loan, they instructed me to take out a credit card as I had never had any debt before and therefore had no credit history.

Reducing or, even better, eliminating your current debt now will better prepare you for when you apply for a home loan. Strategizing how best to make your repayments plus increasing your savings can be a daunting task. But with a plan in place and strict discipline, it’s not impossible.

Please note, this is general advice only and does not take into account your personal circumstances. If you would like to find out the best strategy for you, or if you would like some extra tips, contact Quill today and start building your house deposit!

I was interested but not necessarily surprised to read two articles this week relating to financial fortunes of the general Australian population. The first article talked about financial literacy, where a study by Zurich and Oxford University found that Australia ranked near the bottom of the tables. In the second article, a study by the Actuaries Institute found that almost a third of Australians are in danger of running out of money because they are drawing too much out of superannuation.

With the percentage of Australians that do not currently seek any ongoing financial advice sitting at close to 80%, these reports should not be surprising to anyone. The risk of not achieving any long term goal without some form of coaching, mentoring or external direction is extremely high and it makes sense that those with a trainer, coach or in this case an adviser, have a far better chance of maintaining discipline and achieving their goals.

Why is it that so few Australians reach out for financial advice to help improve their financial literacy?

One of the reasons provided by respondents to many surveys on this subject is that the cost of ongoing advice is just too high and many feel they don’t have sufficient assets to justify the cost. This leads to a situation where those who are in most need of advice are the very ones that don’t receive any. From an adviser’s perspective, the compliance cost of providing advice in the first place drives costs up. Therefore, under the current model, I would argue that this situation is unlikely to improve.

So, what is the solution to increasing the percentages of those that do seek financial advice and thereby starting to redress the issue of poor financial literacy?

This is where I believe the role of automation, in many of the time-consuming back office processes, as well as ‘robo advice’ can make a big difference. These factors can assist advisers to drive down the cost of advice to the end consumer.

I believe that ‘robo advice’ will eventually be embraced by advisers as an opportunity rather than a threat to their profession. It can play a large part in assisting advisers to deliver a ‘bionic’ advice solution to their future generation of clients.

We have already witnessed the start of bionic advice in the US where advisers are able to combine their knowledge and strategic advice in combination with a ‘robo advice’ investment solution. This has assisted in delivering digital advice to a much larger group than otherwise possible under the traditional face to face advice model. My view is that, in doing so, a new generation of adviser will be able to efficiently inform a larger group of clients in a cost effective manner that not only meets their needs but ultimately leads to an improvement in adult financial literacy.

In summary, you don’t need to know and be across all financial jargon. The burden should be on advisers to translate the financial lingo into plain English. New apps like Superstash make this easier. Superstash is like a Fitbit for your super – convenient and game-changing.

It doesn’t matter what sort of entity you are using to run your business. You could be operating as a company, trust or partnership, and your income could still be deemed as Personal Services Income.

Personal Services Income is income that is mainly derived from the personal exertion of an individual.

How do I know if I am receiving Personal Services Income?

To work out if any of your income is Personal Services Income you need to look at each individual income contract and answer the following two questions:

- What percentage of my income relates to personal exertion (i.e. labour – skills, knowledge, expertise, personal efforts of the person performing the work)?

- What percentage of my income relates to materials, supplies and/or tools and equipment used to complete the work?

In answering the above questions, if more than 50% of the income you received relates to personal exertion then this income is Personal Services Income.

Subsequently, if less than 50% of the income received relates to personal exertion then the income is not Personal Services Income. Below is a list of some of the types of income that are not considered Personal Services Income:

- Sale or supply of goods

- Income generated by income-producing assets (i.e. bulldozer hire)

- Income from granting a right to use property (i.e. copyright)

- Income generated by a business structure (i.e. large national professional firm)

Ok, I am receiving Personal Services Income so what does that mean?

Once you have determined that you have received Personal Services Income you then need to work out if the Personal Services Income (PSI) rules apply.

To work out if the PSI rules apply to your business you need to work through the following tests in this order:

-

Results Test – to pass this test you need to meet all of the following conditions:

- Paid to produce a specific result

- Required to provide your own equipment and tools

- Required to fix mistakes at your own cost

If you pass this results test then the PSI rules do not apply. If you do not pass the results test you need to apply the next test which is “The 80% Rule”.

-

The 80% Rule

- Does 80% or more of your PSI come from the same client? If yes, then the PSI rules do apply.

- Does less than 80% of your PSI come from one client? If yes, you need to move on to the remaining tests to figure out if the PSI rules will apply.

-

Remaining tests – Can you pass any one of the following tests?

- Unrelated clients test (is your Personal Service Income from two or more clients who are not connected and did you get the work by making offers to the public)

- Employment test (does your business employ others who produce at least 20% of your principal work)

- Business premise test (at all times of the financial year your business was used mainly for work that generates your PSI, used exclusively for your business, physically separate from your home and physically separate from your clients)

What if I passed the above tests?

If your outcome from the above was that you passed the tests then your Personal Services Income is not subject to PSI rules. This means that you are now classed as a Personal Services Business. As a Personal Services Business, other than reporting certain information in your tax return, there are no other changes to your tax obligations and no changes to the deductions you can claim. Please note: the character of the income has not changed so any profits from Personal Services Income must still be attributed to the individual who performed the service. This must be done, regardless of what type of entity you the Personal Services Business operates from.

What if I didn’t pass the above tests?

If you did not pass the above tests then your Personal Services Income is subject to the Personal Services Income rules which means the following will apply:

- Your business won’t be able to claim certain tax deductions including those listed below:

- a percentage of rent, mortgage interest, rates & land tax even if the business operates from one of the rooms in your house

- payments to associates for support work

- super contributions for associates who do support work

- car expenses for more than 1 vehicle

- The Personal Services Income will need to be attributed to the individual who performed the work as this income cannot be retained in the business

- Your business will need to meet certain tax reporting obligations

- Your business may have additional PAYG withholding obligations

- General Deduction Rule applies. This rule only allows businesses to claim the same deductions that the individual who performed the work could have claimed in the same situation. The expense must be an allowable deduction under tax law and relate to producing the PSI income

This is a complex area and if you have any questions or would like further information please contact our office.

Several months ago, I wrote a blog on the Four Corners episode which brought to light the real need to obtain financial advice when selecting an insurance policy. Just recently, I came across this article in the Sydney Morning Herald which further provides evidence on why you should seek advice. The article titled “Insurer tells family saving daughter’s life is ‘elective surgery’” is worth a read as it touches on the fine print that is often very easily missed but has a big impact on your family’s life should something unexpected arise.

Hold it in your name

I find that, in my profession, a majority of clients hold income protection within their super. As an advisor who is an advocate for life insurance, and in particular income protection, my preference is to always hold an income protection policy in your personal name. There are many reasons for this:

– Premiums are tax deductible

– You are able to access many more features than if you were with 100% super owned policies. This is mainly due to legislation rather than product offerings.

– The policy is portable. This is opposed to holding it in super where you may be required to retain the super fund for the remainder of your working life if you cannot replace the policy.

Make a well-informed decision

Though my preference is to hold the policies personally, I am certainly aware that some people, due to budget constraints, are unable to fund the premiums. This is where you need to consider the pros and cons of super vs non super and weigh up the options that best fit your circumstances. At least then you have the opportunity to make an educated decision.

Changes in Legislation

It should be noted though that since a change in legislation a few years ago, to what policies can be held inside super, we have seen more sophisticated and diverse policies available. While this prevents scenarios such as the Anderson elective surgery dilemma from happening again, not everyone offers these policies. For example, any industry fund does not offer such a policy!

This is just a summarized glance but as you can see life insurance can be a very complex world. This is why it is recommended you obtain professional advice.

How many times have we been out to a meeting, productive or otherwise, and then it’s time to pay the bill. Your colleague reaches over to the check and states, “Don’t worry, it’s on the business today,” but is this expense really a tax deduction?

Matt from Quill helps you learn more about the types of meal expenses that can be deducted in your tax return.