The wide-ranging superannuation reforms come into effect on 1 July 2017. With the changes come a series of issues that Trustees need to be across, even if they don’t immediately affect you or your fund:

Understand the value of assets at 30 June

At 30 June 2017, SMSF Trustees will need to know the total superannuation balance held by members. If you have assets such as real estate in your SMSF, and to an extent other assets such as collectables and artwork, you will need to have a current valuation of those assets. Real estate property values, in particular, may have varied dramatically over the last few years and should be reviewed. The value of the asset needs to be arrived at using a fair and reasonable process. Because of the extent of the changes, it is worth considering the use of an independent and qualified valuer for some assets.

Understanding ‘Total Value’ of your balance

Your total superannuation balance is the total value of your accumulation and retirement phase interests and any rollover amounts not included in those interests. The balance is valued at 30 June each year and it is this value that may determine what you can and can’t do during the following year. For example, if your total super balance is $1.6m or more at 30 June, you are restricted from making further non-concessional contributions in the next year as these contributions may create an excess contribution. And, if your balance is close to the $1.6m cap, then the fund can only accept limited non-concessional contributions.

Self-funded retirees – avoiding adverse tax outcomes

If you are receiving a pension or annuity, a $1.6m “transfer balance cap” applies to amounts in your tax-free pension accounts. The cap is essentially a limit on how much money a member can transfer into or hold in a tax-free account. If you have $1.6m or more in a pension phase account, you will need to reduce the pension value level back below the cap before 30 June 2017. If the excess amount is not removed from the pension phase account the amount will be subject to a transfer balance tax.

If you opt to sell fund assets to manage the cap, transitional capital gains tax relief may be available to manage any adverse tax outcomes.

How do you value SMSF assets?

One of the emerging problems for many superannuation fund members is understanding whether they are close to or are likely to exceed the $1.6m cap at 30 June 2017. For those with assets such as real estate, collectables or art, a current valuation that meets the ATO’s guidelines will be essential. Real estate, in particular, has substantially risen in value in some areas creating uncertainty about the real value.

Fund assets need to be valued at market value. While these assets do not have to be valued every year by an independent valuer, it will be important to have documentation validating the value assigned to the asset. A qualified and independent valuer is recommended if the asset is a significant part of the value of the fund – if the asset is real property, this could be as simple as an online real estate agent.

Should you update your SMSF trust deed?

Over the years, there have been continuous changes in superannuation legislation. While many of these changes do not require you to update your SMSF deed, where a deed has not been updated in at least the last 5 years, we suggest that the deed is updated to ensure it is compatible with current law.

If we have not already contacted you about your fund’s deed, we will be in contact shortly to discuss if an update is required.

As always, before buying, selling, transferring assets, or making any payments, make sure your trust deed allows you to complete the transactions in the way you intended.

Salary sacrificing concessional super contributions

If you have entered into a salary sacrifice agreement to make concessional super contributions, you will need to review these agreements to ensure your concessional contributions do not exceed the new $25,000 from 1 July 2017.

Two hundred outlaw motorcycle gang members have been served notices by the Australian Taxation Office (ATO) for failing to comply with their tax obligations.

There are not a lot of details about exactly what type of income the ATO is targeting but tax law does not differentiate between legally and illegally earned income: if you earn income, you pay tax. Simple.

An English tax law case back in 1886 set the precedent with Justice Denman stating, “In my opinion, if a man were to make a systematic business of receiving stolen goods, and to do nothing else, and he thereby systematically carried on a business and made a profit of 2,000 per year, the Income Tax Commissioners would be quite right in assessing him if it were in fact his vocation.”

The difference between legally and illegally derived income is that you can’t claim losses or expenses if you have been convicted of an indictable offence related to that business activity.

The operation targeting the bikers is part of a joint taskforce with the Australian Federal Police. Data matching technology in recent years has helped identify movements of cash and income from undeclared, and often, illegal activities. The ‘follow the cash’ philosophy works well and often results in frozen bank accounts, disrupted cash flows and supply chains, which impacts on the overall viability of illegal activities.

Anyone with investment property in Australia is probably feeling a little edgy with all the recent media attention on deductions, affordable housing, and negative gearing. We take a look at some of the key tax issues for investors pre and post 30 June:

No more deductions for travelling to and from your investment property

The days of writing-off the costs of travel to and from your residential investment property are about to end. From 1 July 2017, the Government intends to abolish deductions for travel expenses related to inspecting, maintaining, or collecting rent for a residential rental property.

Depreciation changes and how to maximise your deductions now

Investors who purchase residential rental property from Budget night (9 May 2017, 7:30pm) may not be able to claim the same tax deductions as investors who purchased property prior to this date. In the recent Federal Budget, the Government announced its intention to limit the depreciation deductions available.

Investors who directly purchase plant and equipment – such as ovens, air conditioning units, swimming pools, carpets etc., – for their residential investment property after 9 May 2017 will be able to claim depreciation deductions over the effective life of the asset. However, subsequent owners of a property will be unable to claim deductions for plant and equipment purchased by a previous owner of that property. If you are not the original purchaser of the item, you will not be able to use the depreciation rules to your advantage. This is very different to how the rules work now with successive owners being able to claim depreciation deductions.

Investors will still be able to claim capital works deductions including any additional capital works carried out by a previous owner. This is based on the original cost of the construction work rather than what a subsequent owner paid to purchase the property.

There are very limited details about how this Budget announcement will work but we will bring you more as soon as we know.

Business as usual for pre 9 May investment property owners

If you bought an investment property recently, are about to renovate, or have not had a depreciation schedule completed previously, you should consider having one completed.

As a property gets older the building and items within it wear out. Property owners of income producing buildings are able to claim a deduction for this wear and tear. Depreciation schedules are completed by quantity surveyors and itemise the depreciation deductions you can claim.

Higher immediate deductions for co-owners

It’s not uncommon to have multiple owners of an investment property. Co-ownership can, in some circumstances, quicken the rate depreciation deductions can be claimed for the same asset. This is because depreciation is claimed on each owner’s interest. If an owner’s interest in an asset is less than $300, they can claim an immediate deduction. In a situation where there are two owners split 50:50, both owners could potentially claim the immediate deduction, bringing the total immediate deduction available up to $600 for a single asset.

The same method can be used when applying low-value pooling. Where an owner’s interest in an asset is less than $1,000, these items will qualify to be placed in a low-value pool. This means they can be claimed at an increased rate of 18.75% in the first year regardless of the number of days owned and 37.5% from the second year onwards.

In a situation where ownership is split 50:50, by calculating an owner’s interest in each asset first, the owners will qualify to pool assets which cost less than $2,000 in total to the low-value pool.

The value of renovations

It’s best to get a depreciation schedule completed before you start renovations so the scrap value of any items you remove can be recognised and written-off as a 100% tax deduction in the year of removal. This is available for both plant and equipment depreciation and capital works deductions. When new work is completed as part of the renovations (i.e., a new roof, walls, or ceiling), this can also be depreciated going forward.

In some circumstances, there may be depreciation deductions available for renovations completed by a previous owner.

Deductions for older properties

Investors in older properties may still be able to claim depreciation costs. This is because a lot of the items in the house will not be the same age as the house or apartment. Hot water systems, ovens, carpets, curtains etc., have probably all been replaced over time. Additional works, extensions or internal refurbishments may also be deductible.

Further restrictions on foreign property investors

We have seen a number of measures over the years restricting access to tax concessions for foreign investors, particularly for residential property investments. The recent Federal Budget goes one step further, restricting access to tax concessions, increasing taxes, and penalising investors who leave property vacant.

Measures include:

Charge for leaving properties vacant

Foreign owners of residential Australian property will incur a charge if their property is not occupied or genuinely available on the rental market for at least 6 months each year. The charge, which is expected to be at least $5,000, does not appear to apply to existing investments but those made on or after Budget night, 7:30pm on 9 May 2017.

Excluded from main residence exemption

Foreign and temporary residents will be excluded from the main residence exemption. The main residence exemption excludes private homes from capital gains tax (CGT). Existing properties held prior to 9 May will be grandfathered until 30 June 2019. However, it remains to be seen whether partial relief will be available to those who have been residents of Australia for part of the period they owned the property and whether this change will apply to Australian residents who were classified as a foreign resident for part of the ownership period.

Increase in CGT withholding tax

When someone buys Australian real property (i.e., land and buildings) they are currently required to remit 10% of the purchase price directly to the ATO as part of the settlement process unless the vendor provides a certificate from the ATO indicating that they are an Australian resident. These rules do not currently apply if the property is worth less than $2 million. From 1 July 2017, the CGT withholding rate under these rules will increase by 2.5% to 12.5%. Also, the CGT withholding threshold for foreign tax residents will reduce from $2 million to $750,000, capturing a much wider pool of taxpayers and property transactions.

Rules tighten for property purchased through companies or trusts

Australian property held through companies or trusts by non-residents or temporary residents is also being targeted by expanding the principal assets test to include associates. The move is to prevent foreign residents avoiding Australian CGT liability by splitting indirect interests in Australian real property.

Level of foreign investment in developments capped

A 50% cap is being placed on foreign ownership in new developments.

The push for affordable housing

The Government is very keen to ensure that investment is directed into ‘affordable housing.’

The 2017-18 Budget announced an increase in the CGT discount for individuals who choose to invest in affordable housing. The current 50% discount will increase by 10% to 60% for Australian resident individuals who elect to invest in qualifying affordable housing.

In addition, the Government is creating investment opportunities for Managed Investment Trusts (MIT) to set up to acquire, construct or redevelop property to hold as affordable housing. In order for investors to receive concessional taxation treatment through an MIT, the affordable housing must be available for rent for at least 10 years. For foreign investors, MITs are one area where the Government is actively encouraging participation rather than restricting it.

Tax time is almost upon us so it’s time to get prepared. Here’s your tax planning guide including an update of what’s changing this year, to help you get EOFY ready.

Update: Tax Planning 2020 Guide – Individual Tax Deductions

In this guide:

- Income tax changes for 2016/17

- General year end tax planning strategies

- Income tax changes – small businesses

- Income tax changes – individuals

- Superannuation – relevant thresholds

Income Tax Changes for 2016/17

Several tax changes apply in the 2016/17 income year. A brief summary is provided in this guide.

There may be some advantages in acting on some of these items before 30 June 2017.

If you think any of these changes may affect you, please contact us for more details.

General Year End Tax Planning Strategies

Here are a few strategies to consider before finalising your tax this year.

Definition of small business

The definition of a Small Business (SBE) has changed from having $2 million in turnover to $10 million in turnover. Many more businesses will now have access to the SBE tax concessions.

Business income and expenses

Subject to cash flow requirements, consider deferring income until after 30 June, especially if you expect lower income for 2017/18 compared to 2016/17.

Most businesses are taxed on income when it is invoiced. Some small businesses may be taxed only when income is received. Income from construction contracts is generally taxed when progress payments are invoiced or received.

Ensure that you have complied with the requirements to claim deductions in 2016/17:

- Bad debts must be written off in your accounts before 30 June

- Employer and/or self-employed superannuation contributions must be paid to, and received by, the super fund before 30 June and must be within the contributions cap ($35,000 for individuals aged 49 or over on 30 June 2017, otherwise $30,000)

- Depreciation can be claimed for assets first used, or installed ready for use, before 30 June

- Small businesses (turnover less than $10 million) can claim expenses prepaid up to 12 months in advance – for larger businesses, this is generally limited to expenses below $1,000

- Wages paid to your spouse or family members must be reasonable for the work performed.

Small businesses planning major purchases or replacements of capital equipment should contact us for advice. Careful timing of those transactions can result in substantial tax savings.

Review valuations of trading stock in the lead up to 30 June. Best practice is generally to value stock at the lower cost or market selling value. This may change if you expect a tax loss for 2016/17, or substantially higher income in 2017/18 compared to 2016/17.

Personal income, deductions and tax offsets

Subject to cash flow requirements, set term deposits to mature after 1 July, rather than before 30 June.

Consider realising capital losses if you have already realised capital gains on other assets during 2016/17. Conversely, consider realising capital gains if you have unrecouped capital losses, especially if you expect substantially higher income in 2017/18 compared to 2016/17.

If you expect lower income in 2017/18 due to retirement or any other reason, consider deferring income until after 1 July, when you will be in a lower tax bracket. If you are a primary producer and you expect a permanent reduction in income, consider withdrawing from the income averaging system.

Access to the Net Medical Expenses Tax Offset is restricted to medical expenses relating to disability aids, attendant care or aged care.

Arrange for deductible donations to be grouped in the higher income year, if you expect substantially higher or lower income in 2017/18 compared to 2016/17. Make all donations in the name of the higher income earner.

If you plan to purchase income-producing assets, consider acquiring assets that will generate positive cash flow in the name of the lower income earner. Conversely, consider acquiring negatively geared assets in the name of the higher income earner.

Residency changes

Contact us for advice if you have moved to or from Australia for an extended period. You may need to review your residency status for tax purposes. There are important tax consequences if you change residency.

Trusts

Trustees of trusts should ensure that all necessary documentation is completed before 30 June, where you intend to stream capital gains or franked distributions to specific beneficiaries.

Family discretionary trusts may need to make a family trust election if the trust has unrecouped losses, or has beneficiaries whose total franking credits for the year may exceed $5,000.

Tax shelter schemes

Be sceptical of year-end tax shelter schemes. You should not enter a scheme without advice regarding both its tax consequences and commercial viability.

Income Tax Changes – Small Business

Tax rate

The tax rate for small business entity (SBE) companies is 27.5% from 1 July 2016.

Individual small business taxpayers are entitled to 5% discount of the income tax payable on the business income received from a small business entity (other than a company), up to a maximum of $1,000 a year.

Accelerated Depreciation

An immediate deduction is available for an asset costing less than $20,000 acquired on or after 12 May 2016 and first used or installed ready for use between 12 May 2016 and 30 June 2017.

The balance of the general small business pool is also immediately deducted if the balance is less than $20,000 at 30 June.

Blackhole Expenditure

From 1 July 2016, start-up companies, trusts or partnerships can immediately deduct a range of professional expenses associated with starting a new business (e.g. professional, legal and accounting advice). This only applies to SBE’s.

Income Tax Changes – Individuals

Car expenses

From the 2015/16 tax year, the 1/3 of actual expenses and the 12% of original value method for claiming work related car expenses can no longer be used.

A single flat rate of 66 cents per kilometre is to be used for the cents per km method. Alternatively, a log book must be maintained for a 12 week period to determine the business percentage of all running costs.

Zone tax offset

From the 2015/16 tax year, the zone tax offset excludes ‘fly-in fly-out’ and ‘drive-in drive-out’ workers where their normal residence is not within a ‘zone’.

Superannuation – relevant thresholds

Super co-contribution

Super co-contribution helps eligible people boost their retirement savings.

If you’re a low or middle-income earner and make personal (after-tax) contributions to your super fund, the government also makes a contribution (called a co-contribution) up to a maximum amount of $500.

The full co-contribution rate applies for income up to $36,021 and the partial co-contribution applies for income up to $51,021 for the 2016/17 tax year.

Concessional Contributions

The concessional contribution caps for the 2016/2017 tax year are:

- $30,000 for people aged up to 48 years or under as at 30 June 2016;

- $35,000 for people aged 49 years and over.

These represent the limit on the amount of contributions you can make within the year, and include the Super Guarantee payments made on your behalf by your employer.

Should you wish to discuss your superannuation needs, please contact the team at Superfund Partners.

For help with any of the above information in our guide above, reach out and we’ll happily talk you through it step-by-step

No doubt you have already heard about the introduction of a $1.6 million transfer balance cap from 1 July.

When most people see that figure, they think of the asset balance in their account based pensions.

But did you know that this ‘transfer balance cap’ also includes a notional value for every income stream you receive via the superannuation system?

This includes:

- lifetime pensions, including the majority of defined benefit pensions commenced at any time (eg. Commonwealth or State Government defined benefit pensions)

- Complying lifetime annuities

- Complying life expectancy annuities and pensions

- Term allocated annuities and pensions (ie Market linked pensions).

It is important to remember that if you have a defined benefit pension you may need specialist advice to ensure that your account based pension/s are reduced by enough to bring you under the cap.

Therefore, please contact us immediately if you have one of these income streams, and/or have one or more account based pensions totalling $1.6m or more in value, and would like us to review your situation.

After months of speculation as to what the Government is planning to implement in the 2017 Federal Budget, finally, the budget changes have been released to the public. Implementation of changes is soon to commence.

There are certainly some “winners” and “losers” but overall, the aim of the budget is to positively impact our economy. And with a thriving economy, all Australians are winners.

As a millennial, my biggest focus around the budget is; housing affordability and student debt. So, let’s focus on these points.

First Home Buyers

There had been speculation over the previous months that the government was going to allow first home buyers access to their superannuation savings to fund their house deposit. Personally, I was horrified to hear this was a serious consideration. Such a scheme would influence further implications and retirement unaffordability issues down the track. Pleasing to hear, this scheme was dismissed.

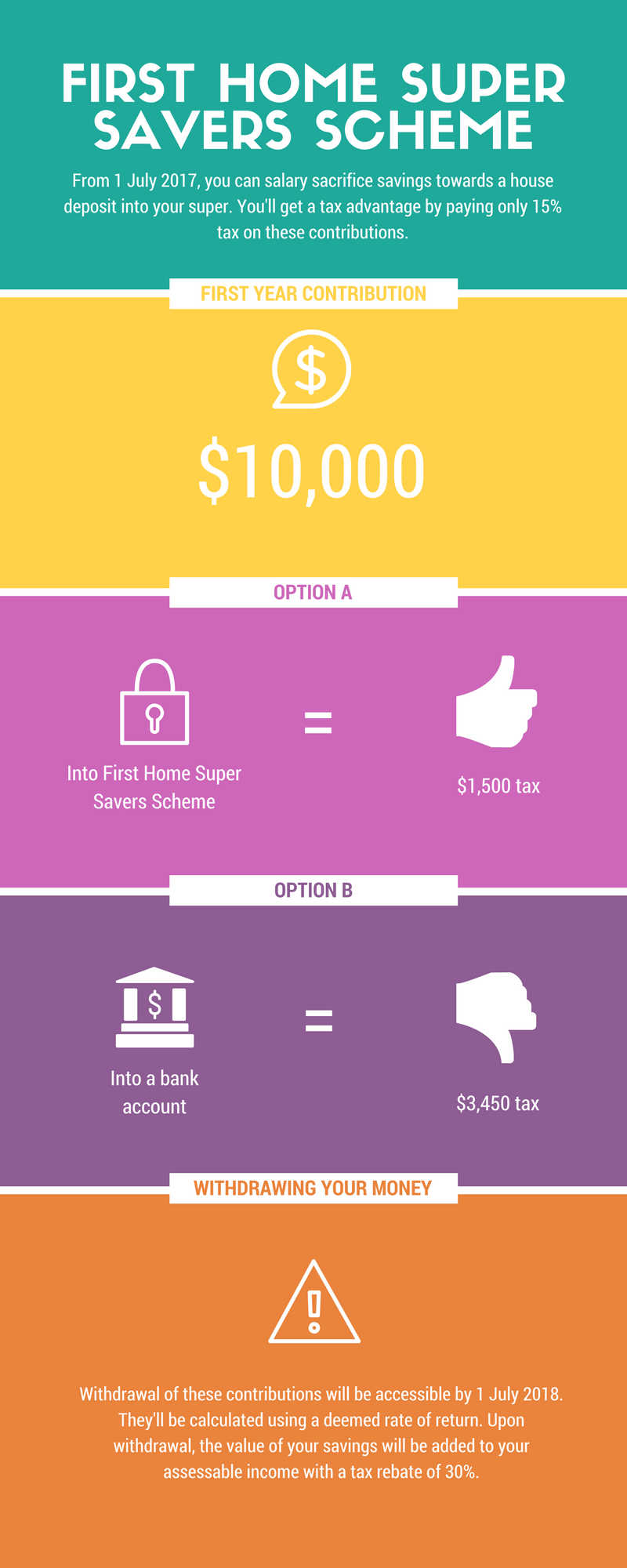

The “First Home Super Savers Scheme” is being implemented from 1 July 2017. This effectively allows individuals to salary sacrifice savings towards a house deposit into their super. By salary sacrificing, a tax advantage is applied as these contributions are considered concessional contributions (pre-tax). Therefore, salary sacrificed contributions and earnings in super are taxed at 15% rather than the marginal tax rate.

Only the contributions to the First Home Savers Scheme will be available to withdraw for first home deposits. Until a condition of release is met, no other superannuation savings are accessible. If you do not end up purchasing a home, these additional contributions will not be accessible until retirement or a condition of release has been met.

It is important to note; the First Home Super Savers Scheme is capped at $30,000. However, as previously mentioned, these contributions are classified as concessional contributions which oblige to the annual cap of $25,000. Noting also that your Superannuation Guarantee Contributions also fall under this cap, you are limited to contributing a maximum of $15,000 (without exceeding the $25,000 cap) into the First Home Super Savers Scheme per annum.

15% tax is applied on each contribution into your First Home Super Savers Scheme account. For example, let’s say you contribute $10,000 in a financial year, only $8,500 hits your first home savers account as $1,500 of the contribution is paid in tax. As a comparison, let’s say you fit into the 34.5% tax bracket and decide to place this $10,000 pre-tax money into a bank account outside of super. This means you will pay $3,450 in tax opposed to $1,500.

Withdrawal of these contributions will be accessible by 1 July 2018 and will be calculated using a deemed rate of return. Upon withdrawal, the value of your savings will be added to your assessable income with a tax rebate of 30%. Therefore, if we use the same example above and assume with the withdrawal added to your assessable income that you remain in the 34.5% tax bracket, you will be liable to pay a further 4.5% tax on the withdrawal of your savings. It feels a bit like the government is double dipping here… nonetheless, it’s still a great tax saving strategy. For a detailed example of how the deemed rate and tax rebate is calculated, refer to Mark Beveridge’s blog.

Although the First Home Super Savers Scheme is capped at only $30,000, I think it’s a great opportunity to start saving. The government has provided a handy estimator tool to calculate the difference in savings when using the First Home Super Savers Scheme verses saving in a standard deposit account outside of super.

Investment Properties

Good news for some property investors! In a bid to make housing more affordable and appealing to Australian investors, the Capital Gains Tax (CGT) discount has increased from 50% to 60%. To be eligible for the 60% CGT discount, the residential property must;

- Be rented to low to moderate income tenants

- Be rented at a discounted rate

- Be managed through a registered community housing provider, and

- Held for a 3-year minimum.

During periods where the property is not used for affordable housing purposes, the additional discount will be pro-rated.

Unfortunately for property investors, reductions and eliminations of certain claimable tax deductions will be implemented. These changes affect previously claimable travel expenses and property plant and equipment depreciation deductions.

Not so great news for foreign property investors, but good news again for Australian investors as these new changes will provide Australians with increased opportunity to invest. Foreign ownership will be restricted to 50% in new property developments. They will also be liable to a minimum $5,000 annual levy if their properties are found to be unoccupied or not genuinely available to rent for at least 6 months per annum.

CGT main residence exemption will also no longer be available for foreign property owners. However, a grandfathering rule for the exemption will be implemented for existing owners up until 30 June 2019.

Foreign tax residents will also see the CGT withholding rate increased from 10% to 12.5% and the property value threshold will reduce from $2 million to $750,000 from 1 July 2017.

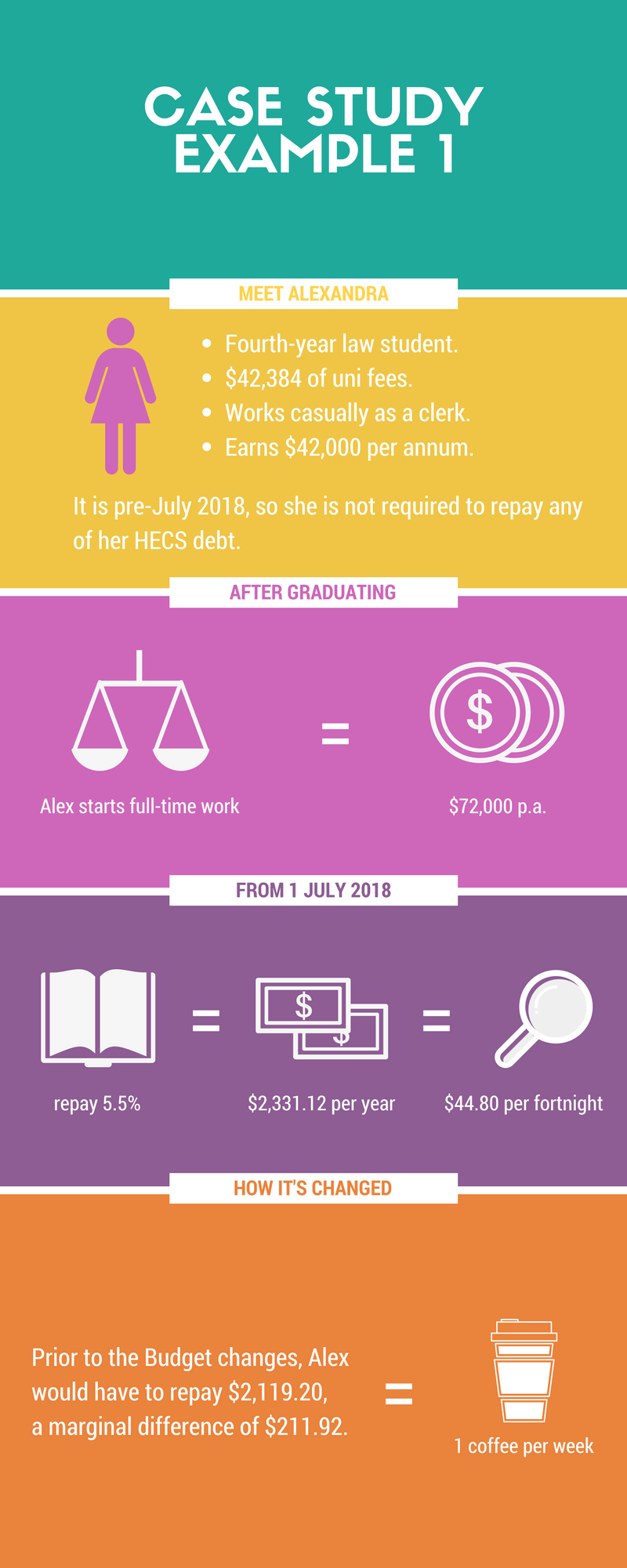

Student Loans

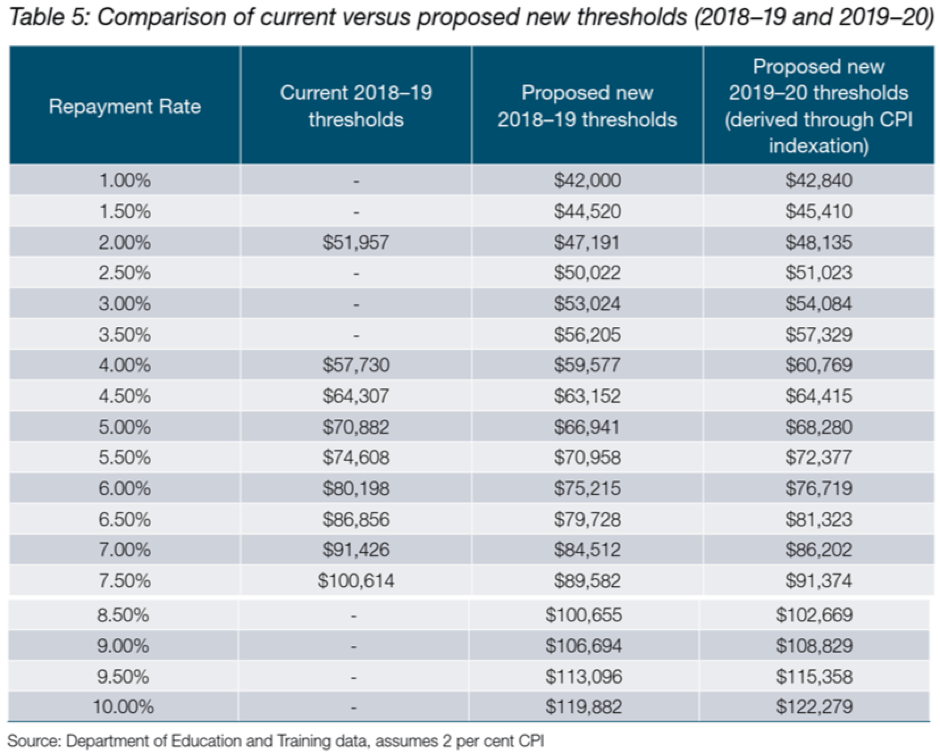

Bad luck for students. It seems to be getting progressively harder to afford study. Not only are university fees increasing, but the minimum income threshold to repay your HECS or HELP debt is now reduced to $42,000 per annum from $54,869 per annum.

Combine that with the average four-year course increasing in fees by approximately $2,200 to $3,600, it’s a scary outlook for existing and future students.

However, we can catch our breath (just a little). It’s not as bad as it sounds. Previously, once the threshold of $54,869 was reached, 4% of the course repayment was due payable. With the new minimum threshold reduction, only 1% is payable with annual income of $42,000. Once your salary reaches approximately $53,000 to $56,000, which is around the old threshold, you will be repaying between 3% and 3.5%.

Let’s do a case study or two to delve into this a little deeper.

It’s important to remember that although there is no interest accumulating on these student loans, they do increase with CPI (Consumer Price Index).

The increase in university fees and reduction in the repayment threshold isn’t the outcome any student was hoping for. But, as detailed in our first case study, the difference is about two cups of coffee (if that!) each fortnight. We will prevail!

Refer to the Department of Education’s comparison table below for more information;

Current 2016-17 Repayment Income Thresholds and Rates:

| Repayment Income | Rate |

| Below $54,868 | NIL |

| $54,869 to $61,119 | 4.00% |

| $61,120 to $67,368 | 4.50% |

| $67,369 to $70,909 | 5.00% |

| $70,910 to $76,222 | 5.50% |

| $76,223 to $82,550 | 6.00% |

| $82,551 to $86,894 | 6.50% |

| $86,895 to $95,626 | 7.00% |

| $95,627 to $101,899 | 7.50% |

| $101,900 and above | 8.00% |

These changes are yet to be legislated, but if you would like to start planning or find out how it will affect you personally, call Quill today.

House Sale Proceeds for Over 65s

Let’s briefly touch base on this also, as you can pass on your knowledge to a family member which this may apply to. Previously, a person aged over 65 was unable to make any super contributions unless they were ‘gainfully employed’ and age 75 was the absolute cut-off age, even if they continued to work. However, with these new budget changes, individuals over age 65 can contribute up to $300,000 of their family home sale proceeds into their superannuation. However, conditions apply as they must have owned the family home for a minimum of 10 years. Fortunately, this type of contribution is not subject to the new $1.6 million superannuation caps.

There are also Centrelink implications to consider for those receiving a part pension under the assets test. If they sell down their home and contribute the funds into their super or retain it outside of super, they could see a reduction or elimination of their part pension. If this could affect someone you know, they can contact Quill to discuss their circumstances.

By now, most are aware that the Federal Court ruled that the provision of transport by an Uber driver to an Uber rider is the supply of ‘taxi travel’ for the purposes of the GST Act, therefore requiring Uber drivers to be registered for GST.

The Fringe Benefits Tax (FBT)

Due to the complexities of our tax system, this ruling only applies to the GST Act, so how does the Fringe Benefits Tax Assessment Act apply to Uber travel and why does this matter? If you provide taxi travel to your employees and that travel begins at or ends at your employee’s place of work, or is provided as a result of sickness or injury, section 58Z of the FBT Act exempts the provision of that travel. So, if that travel is not deemed to be ‘taxi travel’, FBT may apply to the provision of that benefit.

Under section 136 of the FBT Act, a ‘taxi’ is defined as a motor vehicle that is licensed to operate as a taxi. Where vehicles used by Uber drivers are not subject to a taxi licensing regime, the travel provided by those vehicles may not qualify for the exemption.

To operate as a ‘taxi’ in Queensland, providers are required to have a taxi service licence. The licence authorises the holder to provide a taxi service in a specific area subject to certain conditions. These licences can only be obtained by buying or leasing an existing Taxi Service License or by tendering for new Taxi Service Licenses if and when they become available through public tender. The license holder, among other criteria, must hold driver authorisation which is also a requirement to be an Uber driver. Furthermore, there are requirements that do not apply to Uber drivers such as not picking up within another Taxi Service Area, displaying a distinctive registration plate and having a taximeter fitted to the vehicle.

The lowdown on FBT

It appears that in Queensland, Uber drivers, whilst requiring driver authorisation and annual safety inspections, are not licensed taxi service providers. Under the current FBT Act, it appears that Uber travel in Queensland may not be eligible for the taxi travel exemption. The state governments legislate taxi service licensing and therefore varying tax treatments among the states may apply.

When determining your liability to Fringe Benefits Tax, you should consider benefits provided by way of Uber travel.

The ATO has issued an information sheet to let taxpayers know that money earned from renting out a room in a house is rental income.

This applies to rooms rented by traditional means or through a sharing economy website or app.

Also, taxpayers can only claim expenses related to the part of the house they rent out (so expenses will need to be apportioned accordingly).

Example: renting out part of a unit or house

The following example illustrates how the ATO would expect rental deductions to be calculated.

Jane has a two-bedroom unit with two bathrooms. She lives alone and only uses her spare room as an occasional home office, for storage and when she has guests.

Jane mainly uses the ensuite bathroom. The second bathroom is accessible from the main areas and mainly used by visitors.

Jane decides to rent out the spare room on a sharing economy website to earn extra income.

When paying guests come to stay, Jane removes all excess items from the room and does not access the area.

She also gives paying guests access to common areas including the second bathroom, kitchen, living area and balcony, and to her wi-fi. For the period guests are staying and have access to these, Jane can claim 50% of associated costs.

Jane had the room available and occupied 150 days in the year. When she is not renting out the room she uses it as storage and a home office.

Claiming Rental Deductions

Jane calculates what she can claim based on the following additional factors:

- The room is 10 square metres

- The house is 80 square metres

- The common areas are 50 square metres

She works out she can claim 17.9% oI her general expenses (such as electricity, interest on her mortgage, internet expenses, rates and body corporate fees) after adding the following two calculations together:

- room occupancy:

(10/80 x 150/365) x 100 = 5.13% - common areas:

((50/80 x 1s0/365) x 50%) x 1oo = 12.84%.

She can claim 100% of the expenses associated solely with renting out the room, such as the facilitator’s commission or administration fee.

Note: that CGT may also apply if a property used to generate rental income is sold.

The ATO has released a public taxation ruling covering the ATO’s views on the deductibility of expenditure incurred in acquiring, developing, maintaining or modifying a website for use in the carrying on of a business.

Importantly, if the expenditure is incurred in maintaining a website, it would be considered ‘revenue’ in nature, and therefore generally deductible upfront.

This would be the case where the expenditure relates to the preservation of the website and does not:

- alter the functionality of the website;

- improve the efficiency or function of the website; or

- extend the useful life of the website.

However, if the expenditure is incurred in acquiring or developing a commercial website for a new or existing business, or even in modifying an existing website, it would generally be considered capital in nature (in which case an outright deduction cannot be claimed).

Example 4 from the ATO Website – existing business establishes a basic website

62. Eve has owned Fashion from Eden, a suburban boutique for many years. She decides to establish a website and engages a web developer. The developer sources the domain name designs the website and arranges web hosting. The total establishment cost is $2,500. Eve makes a series of progress payments while the website is being constructed. Additionally, the web developer agrees to make content updates as needed. Eve’s regular ongoing costs are domain name registration and server hosting.

63. The website is a single page, containing:

the business name and contact details,

opening hours,

some promotional text identifying clothing brands sold,

a subscription facility for promotion and sales emails, and

links to the business’s social media pages.

64. There is no online sales facility. The website requires updating only when the business’s details change. In 2015, the business wins a local business award and has the website content updated to display this.

65. The website is an enduring feature of the business, established to promote the business in new markets and attract new customers. It is more than a transitory advertisement; it is a modern equivalent of a hoarding. The expenditure incurred to create the website is a capital expense. The progress payments retain their capital nature despite the payments being made by instalments. However, any developer fees for content updates with transitory benefits, such as the reference to the local business award, are of a revenue nature.

66. The website is a depreciating asset; it is software used by the business in the business to perform the function of increasing brand awareness. It is ‘in-house software’ and depreciable under the capital allowances provisions. (Return to paragraph 19 of this draft Ruling)

You can find more examples and all the details of the ruling here. Please contact us here at Quill for further assistance.

Concessional contributions are those made with pre-tax income and can come in many forms, most commonly as

- Superannuation Guarantee contributions made by your employer,

- Salary sacrificed contributions made on your behalf, or

- Tax-deductible contributions if you are self-employed.

Below, we’ve summarised a few important considerations regarding the cap changes that became law on 29 November 2016.

-

A lower cap will apply from 1 July 2017

As part of the 2016 Federal Budget, the Coalition government announced plans to reduce the annual concessional contribution cap to $25,000 from 1 July 2017. The new cap will now apply to everyone regardless of age.

This will see the lowering of both the over-50s concessional (before-tax) contributions cap of $35,000 and the general concessional contributions cap (for under-50s) of $30,000. However, it’s important to note that the $35,000 and $30,000 caps still apply for the current (2016/2017) financial year.

-

Making the most of your caps

If you are looking to increase your pre-tax contributions to superannuation, now is a good time to ensure that you are making the most of your concessional contribution cap. This may involve investigating a salary sacrifice arrangement with your employer or reviewing an existing arrangement before the cap decreases in July. But it is equally important to ensure that you take action from 1 July 2017 to plan for the lower cap in the 2017/18 financial year.

Another important change to note is that from 1 July 2017, anyone who is eligible to make voluntary super contributions will also be eligible to make personal concessional (tax-deductible) contributions. Currently, people earning more than 10% of their income as an employee (i.e. salary and wages) cannot make a tax-deductible super contribution, so this recent change should provide greater flexibility with:

- end of year super top-ups by making personal concessional contributions to use up any remaining concessional contribution cap;

- deciding how to contribute bonuses, annual leave, and long service leave; or

- tax-effectively contributing lump sum leave payments received upon termination of employment.

-

Future indexation

While we will have to live with lower caps from now on, the government will continue the practice of indexing these in line with average wage growth. Therefore, we can expect the caps to increase every few years in increments of $2,500.

-

Carry-forward concessional contributions

There’s also good news for those with volatile or lumpy income, and those working intermittently. From 1 July 2018 onwards, if you fail to use your annual concessional contributions cap of $25,000, you can carry forward the unused portion for up to 5 years. Carry-forward concessional contributions may assist clients with breaks in employment to make ‘catch-up’ contributions when they return to work.

The provision applies on the condition that your total superannuation balance is less than $500,000 as at 30 June at the end of the financial year immediately preceding the financial year in which the contribution is to be made. Also bear in mind that as this new rule only takes effect from the 2018/19 financial year, you won’t be able to carry forward any unused concessional contributions cap until at least the 2019/2020 financial year.

-

Exceeding the cap

An important consideration is what happens if you do exceed the concessional contribution cap. Since the 2013/14 financial year, excess concessional contributions have not been subject to excess contributions tax. Therefore, if you do exceed the cap, the amount will be included in your assessable income and taxed at your marginal tax rate. In addition, the ATO imposes the Excess Concessional Contributions (ECC) charge so that a person does not obtain a financial advantage due to the delay in payment of tax on their ECC.

The ECC charge period is calculated from the start of the income year in which the excess concessional contributions were made and ends the day before the tax is due to be paid under your first income tax assessment for that year. The ECC charge rates are updated quarterly on the ATO website, with the current rate being 4.76% (Dec 2016 quarter).

What’s next?

So there’s plenty to think about in managing your concessional contributions this year and the next, so why not ask your financial adviser how you can make the most of the new rule changes?