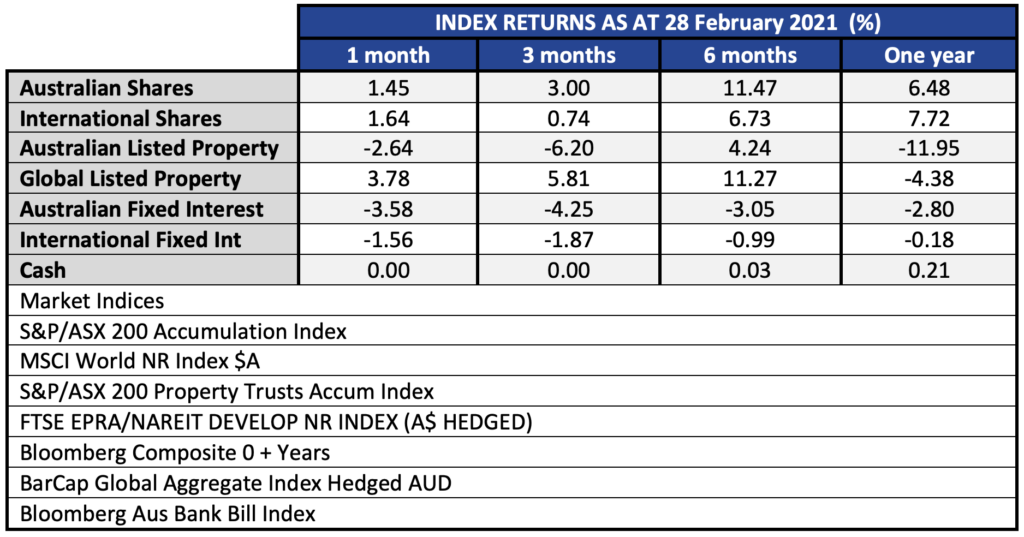

The S&P/ASX 200 Accumulation Index increased +1.45% while the MSCI World Index (A$) was also higher at +1.64%. Both equity benchmarks are now in positive territory on the one-year basis spanning back to 28 February 2020.

The Australian dollar picked up in February, finishing the month up 1.13% vs the USD (0.7696), and 1.35% higher versus the Euro (0.6378).

In January we remarked on the long-term part of the interest rate market, noting that Australian ten year bonds rose from 0.98% to 1.13%. That trend accelerated in February, with the ten year bond yield finishing the month at 1.85%, after briefly touching 1.97% during the month.

In bond portfolios with long maturity durations this creates a temporary, mark-to-market, capital loss. That is reflected in the Bloomberg Composite Bond index posting a loss (-3.58%). Global bonds also posted losses for the month (-1.56%).

The Reserve Bank has so far been focused on the 0 to 3 year part of the yield curve, and towards the end of February stepped up the war to keep rates pinned at close to 0.10%.

Listed property dipped on the higher long term bond rates. The sector was down (-2.64%) however yields remain attractive relative to current interest rates and elevated valuations in growth stocks.

Observing the table above, it is ironic now to see that on a one-year basis – reaching back to pre-COVID – the negative returns are in ‘safe’ fixed income, while the positive returns are in ‘risky’ equities. The outcome is certainly somewhere between ‘our worst fears, and best dreams’ that we talked about back in March 2020 when we suggested that investors avoid over-reacting amid extreme volatility.

If you want to get more involved with your superannuation, investments or insurance, please give us a call at Quill Group.