It continues to be a confusing story when it comes to economic news and share market performance. In a week that produced Australia’s first recession in 29 years and the worst growth result since the end of WW2 one could have been forgiven for thinking that this was bad news for the share market.

However, to the contrary the Australian market continues with its strong path of recovery and is only around 6% below where it was 12 months ago. Meanwhile the broader US market recorded another very strong rise yesterday and the technology heavy NASDAQ recorded yet another record rise.

Lock-downs hampering recovery

There is no hiding the fact that border closures and the Victorian lock down is having a significant impact on the Australian economy and the Federal Government is very keen to see some of these restrictions lifted as soon as possible so that business, domestic tourism and employment prospects can begin a very slow path to recovery.

It must be said however, that the economic situation in Australia is not nearly as bad as many other countries such as the UK with a negative growth June quarter of -21%, Europe -15% and the US –9%. We understand this difference is cold comfort to individuals and businesses currently struggling, however it will hopefully ensure Australia is better placed to recover.

What is driving share market growth?

What is driving the share market recovery in the face of such a poor economic backdrop and an official recession?

The most obvious reason for the relative strength in the share market is simply the flood of liquidity from central banks on a global scale coupled with a very low interest and inflation rate environment.

Another school of thought is with interest rates at near record lows, combined with investors being nervous about short to medium term property prices, many investors have poured into the stock market looking for bargains where companies may have been oversold earlier in the year.

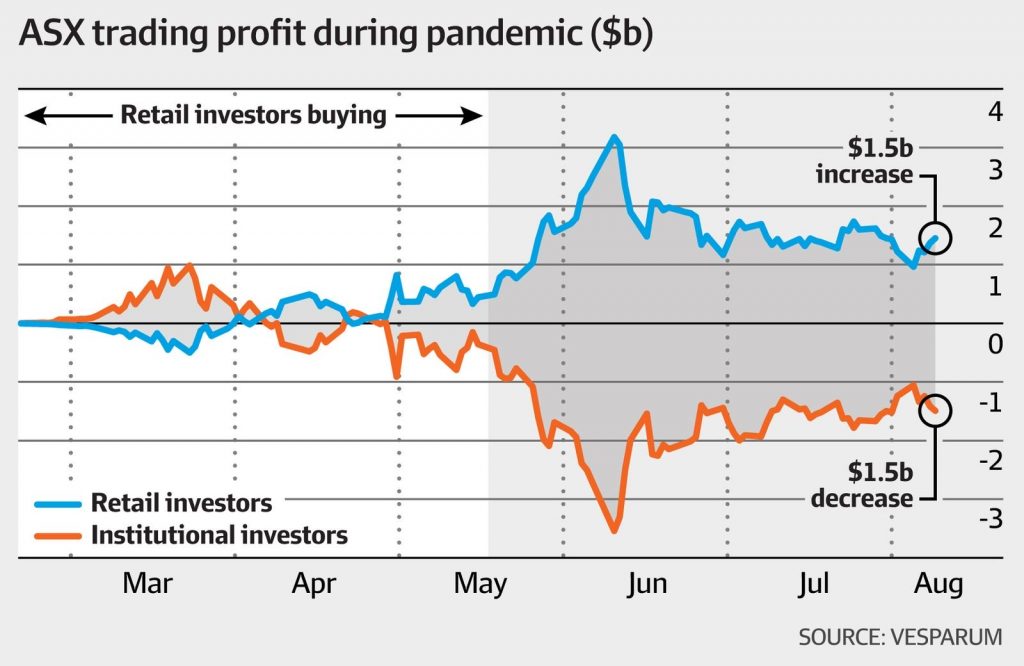

Impact of ‘Robinhood’ investors

In addition to the bargain hunters, there are those looking to take advantage of recent volatility to speculate on growth, particularly through companies with a technology focus. This group has been coined the ‘Robinhood’ cohort, based on the name of a smart phone app that has attracted a large number of millennial investors in the US.

As reported in the Financial Review a few weeks ago, the average weekly value traded through Commsec, has grown almost four-fold, from $1.7 billion before the pandemic to $4.2 billion during the COVID-19 period.

Superannuation changes coming

In other news this week, the Federal Parliament is currently debating two changes impacting superannuation and self-managed super funds (SMSFs).

6 member SMSFs

The first of which is a proposed increase to the number of members allowed in an SMSF from four to six members. This change was announced back in the 2018/19 Budget however never came to fruition.

The overwhelming majority (93%) of SMSFs only have one or two members, typically a couple. The expansion to six members will likely only be taken up by a very small percentage of families, however in the right situation it could transform an SMSF into a powerful multi-generation wealth creation and protection vehicle. If this change becomes law, we will provide a more in depth update on how it can be taken advantage of.

Bring-forward rule extension to age 67

The second and potentially more powerful change currently before the Senate after passing through the House of Representatives last week seeks to extend the age limit for bring-forward non-concessional contributions from age 65 to 67.

Laws recently changed from 1 July 2020 which increased the superannuation work test from age 65 to 67. However, someone who was aged 65 or 66 can still only make a non-concessional contribution of $100,000 without needing to meet the work test. This change will enable someone over 65 (but under age 67) to use the bring-forward rule and contribute $300,000 in one year.

Interestingly, the age at which an individual has full access to their superannuation (regardless of whether they’re still working or not) remains at age 65. This provides a two year ‘magic-window’ where lump sums can be taken and subsequently re-contributed thereby changing ‘taxable’ component monies to ‘tax free’ component amounts which are tax free if passed onto adult children beneficiaries or an estate in the future.

There is no guarantee this change will pass in the current Parliament sitting days, so it could October before it becomes law. When this change happens it will apply from 1 July 2020.

Questions or feedback

There is no doubt we are navigating through uncertain times. If you have any questions in regards to this article, or if you need any clarification, please reach out to me or your Quill Relationship Manager for further information.