If you are thinking about switching your super to cash due to recent market volatility, it’s important to understand that doing so locks-in losses and that even the savviest investors will have trouble figuring out when to re-enter the market so as to fully capture the rebound.

This article was originally published in the Australian Financial Review 14 April 2020. Original article: Want to switch your super to cash? Think again

Should you switch your super to cash?

If you’ve been struck with an overwhelming desire to move your superannuation to cash in the midst of the coronavirus chaos on markets, you’re not alone. In fact, behavioural economists have a name for the phenomenon: prospect theory. Also known as loss-aversion theory, it is the preference to avoid losses more than acquire equivalent gains.

“Put simply, the pain of losing $100 is more pronounced than the joy of making $100,” says Alastair MacLeod, the managing director of boutique asset manager Wheelhouse Partners.

“People spend years crafting a long-term investment strategy which is very outcomes-focused but in a crisis, the plan goes out the window,” he says.

“You feel this need to reach for the phone to call your broker, sell all your shares and move to cash. You feel the weight of this rock bearing down on you and you’ve got to get out from under it.”

When markets crash, investors inevitably feel the need to flee to “safer” asset classes, especially cash.

Crystallising losses

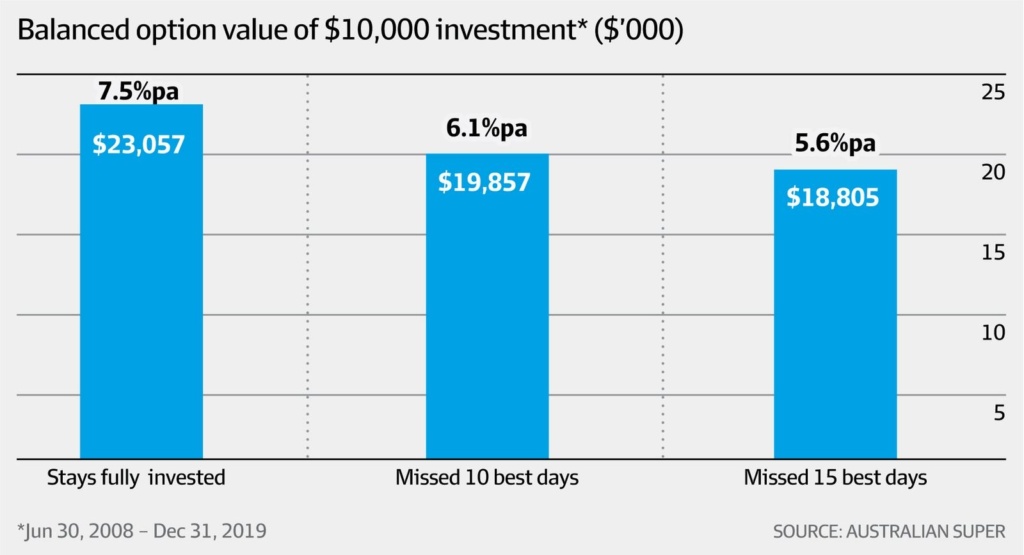

But switching crystallises losses and even the savviest investors will have trouble figuring out when to re-enter the market so as to fully capture the rebound.

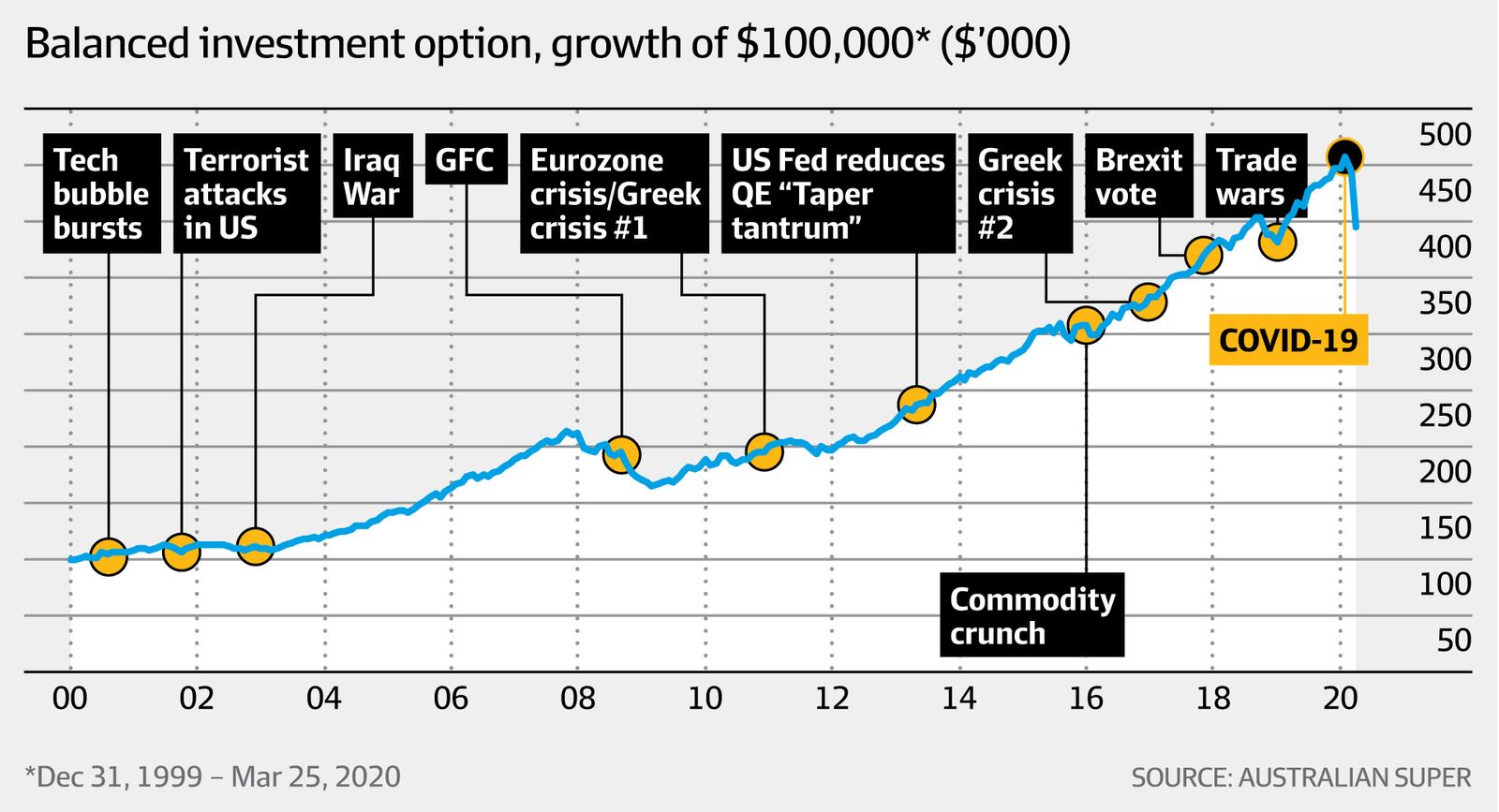

Take these figures from AustralianSuper.

At a conference last year, AustralianSuper chief executive Ian Silk revealed that some members had lost six-figure sums because they had moved their money into cash after the GFC – and left it there.

According to research and ratings agency SuperRatings, the median “balanced” super fund has fallen about 10 per cent for the calendar year to date, and 3.1 per cent for the financial year to date.

SuperRatings defines a balanced fund as one with between 60 per cent and 76 per cent exposure to growth assets.

The median “growth fund”, which has up to 90 per cent exposure to growth assets, is down 14 per cent for the calendar year to date, and 6.4 per cent for the financial year to date.

Sunsuper’s $1.2 billion

“Our message for super members, especially those further from retirement, is stay invested if you can,” says SuperRatings executive director Kirby Rappell.

There are no publicly-available figures on how many super members have switched to more conservative investment options, including cash, since the onset of the coronavirus chaos.

Sunsuper chief executive Bernard Reilly says members of his fund moved about $1.2 billion into cash, conservative and “capital guarantee” options in March.

That equates to about 2 per cent of funds under management.

“We recommend people seek advice before they make a change,” Reilly says.

“Often we’ve had people call up after they’ve made the change wanting to see if they’ve made the right decision or not. And often moving into cash is not the right answer. ”

Of course, everybody’s situation is different and the effects of plummeting equities are felt hardest by those close to retirement and already in retirement.

The combination of sequencing risk and loss aversion is felt especially acutely by retirees, MacLeod says.

“When you’re in retirement, you only have financial capital. So this fear of loss, this loss aversion, is enhanced,” he says.

“But by selling at the bottom when much of the damage has already been wrought, losses can be effectively locked in and longer-term investment outcomes more difficult to achieve.”

Present-day retirees find themselves in a particularly precarious situation, MacLeod adds.

“Typically as you move into retirement, risk is dialled down because you want to preserve capital and you want to increase certainty. A way to do that is to have more income generation.

“But with interest rates at such low levels, retirees have been pushed out on the risk curves to buy more equities.

“I think it’s completely unfair, that older Australians who have spent their life working, and saving to fund their retirement, are now being forced to take on additional risk at precisely when they have the most to lose.”

So, what to do?

For one thing, resist that voice in your head urging you to switch to cash, MacLeod says.

“Recognise what is happening, that this is an emotionally charged feeling, and that abrupt changes to your long-term plan are likely to affect your long-term outcome.

At least until you’ve sought professional advice.

“It is in market downturns that your financial adviser will be of most help. He or she can steady your hand and bring you back to your long-term strategic plan.”

Another tip is to realise these events occur more often than popular discourse suggests, MacLeod says.

“A quick scan of the longer-term history of share markets will show numerous bumps along the way, but it will also very clearly show superior wealth creation over the longer term.

“Life expectancies have been steadily increasing. If we’re living longer, the concept of our capital lasting the distance becomes far more acute. We need portfolios that will last our entire retirement, and at the moment, the yields on cash may struggle to achieve that.”